News

The ASX Small Ordinaries Accumulation Index is having a decent year. At least that's what the headline suggests.

The index is up around 10% this financial year, comfortably ahead of a 5% return for the large-cap skewed All Ordinaries Accumulation Index. Dig a little deeper, though, and the picture looks very different. Small resources stocks have rallied more than 50% and now account for around 35% of the index, well above their historical weighting of closer to 20%. Small industrials, meanwhile, are down around 5%. Technology stocks have fallen almost 30%.

Greed and panic have both been hidden by the average.

Investors have no shortage of concerns. Consumer confidence remains fragile, interest rates have risen sharply and the conflict in the Middle East continues to create uncertainty. The budget adds yet another layer of anxiety into the mix.

Forced sellers, especially of small cap industrials, have been seen around the market recently as some funds face investor redemptions or closure. Tax-loss selling continues to weigh on some stocks as well.

In environments like this, investors often sell first and ask questions later. Smaller companies tend to bear the brunt of that caution. On average, the index sits below its long-term valuation multiples and is unusually cheap relative to larger companies.

In December the Forager Australian Shares Fund held approximately 19% of the portfolio in cash (including a company in the later stages of a takeover).

Today cash sits at about 5%.

Revisiting Technology

Technology has become one of the market's most controversial sectors.

Much of the debate centres on what has become known as the "Saaspocalypse" - the idea that artificial intelligence will permanently damage software businesses by making software development cheaper and reducing barriers to entry.

There is some truth to that concern. Some software companies will struggle. Others, however, may emerge stronger.

The best software businesses solve important problems at a relatively low cost for customers. Catapult (ASX:CAT) is a good example. The company provides wearables and video analysis tools to professional sporting organisations around the world.

For elite clubs spending tens or hundreds of millions of dollars on players, Catapult's average annual spend of around US$30,000 per team is a rounding error. The hardware and software suite helps improve performance, reduce injuries or gain a competitive advantage, so remains very compelling.

After selling out of Catapult as valuations reached stretched levels late last year, the business is now the second-largest investment in the Forager Australian Shares Fund.

Switching costs matter too. Bravura Solutions (ASX:BVS) provides mission-critical software to wealth managers and superannuation funds. These are systems that sit at the heart of client administration and reporting. Replacing them is expensive, disruptive and risky. Trust becomes an important competitive advantage, particularly in heavily regulated industries.

Having also exited Bravura late last year the company is now a top-five investment for the Fund.

Some technology businesses possess moats that extend well beyond software. Hipages Group (ASX:HPG) operates Australia's largest online marketplace connecting tradies with customers. The value lies less in the underlying technology and more in the network itself. Homeowners post jobs because tradies are there. Tradies participate because that's where the jobs are. We have taken the opportunity to increase the Fund’s investment in the business this year.

Since the start of the calendar year the Fund’s software investments have moved from 3% to 16% of the portfolio.

More Capital for Existing Investments

Capital has been deployed across a handful of existing investments outside of software too.

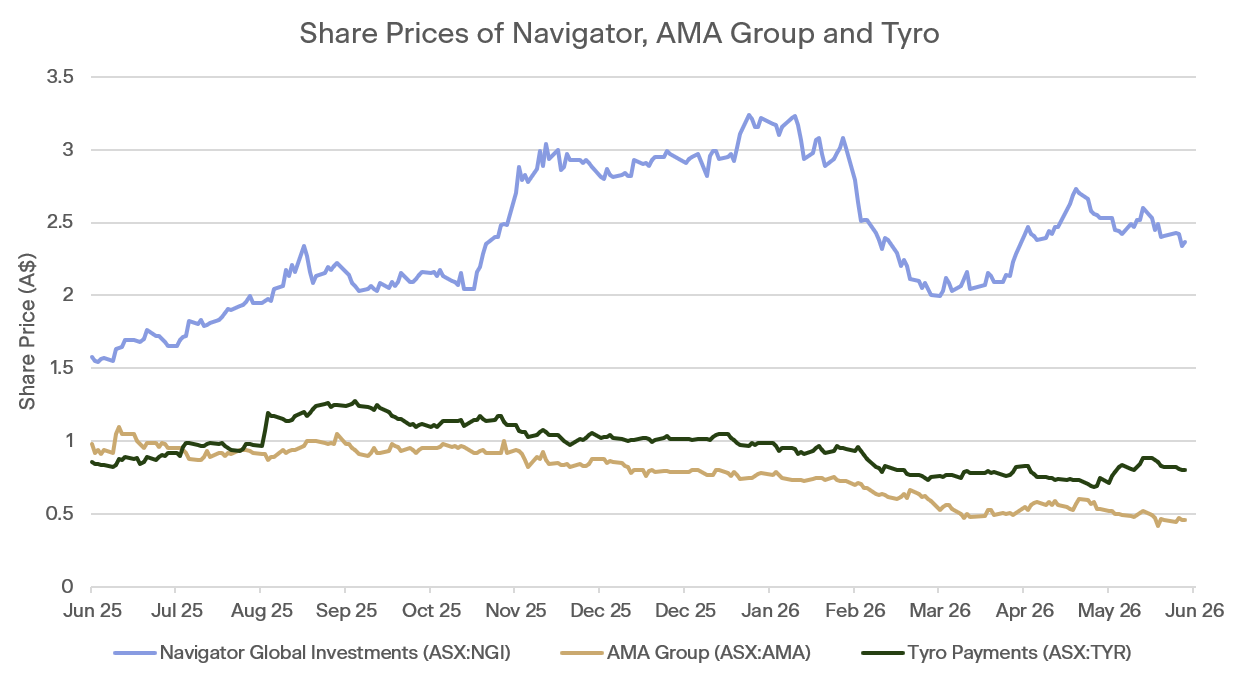

Despite an accretive acquisition, alternative fund manager investor Navigator (ASX:NGI) is down by more than a quarter from prior peaks. The business continues to benefit from growth in assets under management and all-important performance fees, while the acquisition should enhance scale and importantly diversify earnings.

Panel beater AMA (ASX:AMA) showed decent progress in its first three quarters and has maintained guidance despite the threats from higher oil prices. Operational improvements should continue to flow through the business, improving margins over time. The stock is sitting more than 60% below recent peaks.

Payment terminal provider Tyro (ASX:TYR) has been through a few years of regulatory uncertainty. The RBA’s recently released payments review puts Tyro in a good position to gain market share. A new CEO is in place to build on the operational momentum, especially in health and new verticals. The stock is down about 35% from recent peaks.

Source: Bloomberg

The attractiveness of the opportunities available to the Fund is similar to what we saw in late 2022 and early 2023, when sentiment towards small companies was particularly weak. That period of pessimism set the foundations for many years of strong performance.

Takeovers Shine a Light on Hidden Value

Small cap public company investors are not the only potential owners of unloved and underappreciated stocks. The past few weeks have seen takeovers of smaller industrial companies ramp up.

Recreational vehicle operator Tourism Holdings (ASX:THL) saw a bid from a private equity firm, which has paired up with a major shareholder. The first bid came twelve months ago at NZ$2.30 per share. The bid price now is NZ$3.10 per share, and much closer to the board’s view (at the time) of value being “well north of $3.00 per share”.

Readytech (ASX:RDY), enterprise software provider across a few industries, has disappointed investors with slower revenue growth and rising costs over the last few years. The resulting depressed valuation attracted the likes of Topicus (TSX:TOI), a spin-out of Canadian vertical software behemoth Constellation Software (TSX:CSU). The bid, at $2.00 per share for the whole business or $1.75 per share for a minimum of 50.1%, has been rejected by the board. But it does illuminate the strengths of the business, unfortunately hidden under a bloated cost base.

And foreign exchange provider OFX (ASX:OFX), deep into a technology transition while losing market share to competitors, is running a well-progressed strategic review with multiple interested parties. The business retains a valuable client base, licenses around the world, and a new platform. The process is due to complete this month.

As in the past, if public company investors fail to recognise the value on offer, that value can be realised by bidders. More takeovers are likely if the malaise continues.

Markets are rarely comfortable when the best opportunities emerge. Small industrials remain out of favour, technology stocks are being priced as though disruption is inevitable and investors continue to focus on near-term risks. Of course, investing during periods of volatility or when certain sectors are out of favour always carries risks, but from a Forager’s perspective, we believe this environment has opened up some great opportunities in unloved and underappreciated stocks.

Investors wishing to update their Distribution Preferences for the Forager Australian Shares Fund can do so by logging into Automic, selecting "Reinvestment Plans" and following the prompts

Look, I’m not terribly happy about the Capital Gains Tax (CGT) changes proposed in the Budget last week. Like most of you, I feel I already pay more than enough tax.

Nor has any recent iteration of the Federal Government convinced me it spends our tax dollars particularly well. Take the giant hydroelectric “battery” known as Snowy 2.0. Conceived on a coaster in a Cooma pub in 2017, where it should have been swept away at closing time. It was originally slated for completion by 2021 at a cost of $2 billion (lol). The latest schedule says 2030, with a projected cost of $42 billion. Who knows where it ends?

There are roughly 15 million employed taxpayers in Australia. Spread across them, $42 billion works out to about $2,800 each, or $5,600 for a two-adult household. If you work full time and enjoy reading financial blogs, my guess is your share of the bill will be higher. A lot of money for just this one largely-predictable mistake.

Then there’s Inland Rail, long planned to connect Melbourne and Brisbane via inland NSW. It’s now likely to connect Melbourne only to Parkes after the original budget blew out several times over. And it’ll still cost your family a modest holiday’s worth of dollars.

And it’s impossible not to mention the NDIS. Around $50 billion every single year and, until recently, growing at such a pace that it would theoretically have overtaken the entire Australian economy within a few decades. I know deserving recipients who describe it as life changing, and who am I to deny them needed support? But how much needless fraud and waste has occurred under the watch of successive governments? Lax systems, lax oversight, and we’re the ones footing the bill.

All of which is to say: surely there is far more that can and should be done on the cost and efficiency side of the ledger.

I share the concerns about paying more into a system that already struggles to deliver value for money. I also agree with those calling BS on politicians trying to package these changes as a housing affordability measure.

And I have particular concerns about the proposed system’s impact on business formation. Especially the high-risk, high-return entrepreneurial ventures that, given the right nurturing, create the champion businesses of the future. You know, the ones we’ll need for jobs growth and a broader tax base.

With that out of the way, much of the commentary surrounding the proposed CGT changes has focused on extreme outcomes rather than typical ones.

The changes are meaningful, but they will affect different situations very differently — and not always negatively. Outcomes vary enormously depending on the type of investor, the structure they invest through, and the nature of the returns they generate.

Mixed bag

The biggest losers are clearly those pursuing genuinely high-return outcomes over long periods of time. That includes entrepreneurs building successful businesses from scratch, early-stage investors backing riskier ventures, and growth-oriented investors hoping to compound capital materially faster than inflation.

And, yes, that will include many of Forager’s investors, perhaps even you. It also includes me. If you generate good (or better) long-term capital gains, your eventual tax bill is likely to rise significantly under the proposed regime. There’s little point pretending otherwise.

But it’s also worth recognising that most long-run investment returns are not purely capital gains. In Australia especially, a substantial proportion of total equity returns has historically come from dividend income, which continues to receive relatively favourable treatment and is largely unaffected by these proposed changes.

Inflation matters too.

One underappreciated feature of the proposed regime is that it restores the principle that investors should pay tax primarily on real gains rather than purely nominal ones. Under the current system, investors often pay capital gains tax even where much of the “gain” simply reflects inflation over time.

I’ve long argued that the 1999 CGT changes created a particularly harsh outcome for more conservative investors willing to accept lower returns. Assets compounding at or below the inflation rate can generate meaningful tax bills under the current regime despite little or no real wealth creation. That wasn’t the case prior to 1999.

Under the proposed system, those investors will likely end up better off.

In fact, investors can even outperform inflation modestly and still be better off under the proposed rules.

A lukewarm example

To illustrate, take the past 10 years of returns from the iShares Core S&P/ASX 200 ETF, a widely held ETF providing exposure to a broad portfolio of Australian businesses. Over the decade to 30 April 2026, it returned 9.21% per annum — broadly in line with long-run equity return expectations.

Of that 9.21%, 4.70% came from capital growth, with the remaining 4.51% from distributions. Most of those distributions ultimately reflect dividends paid by the underlying companies. Australian dividends already receive relatively favourable tax treatment through franking credits and are unaffected by the proposed changes.

Now consider the tax implications of that 4.70% annual capital growth, assuming the investment was held for a decade and then sold. Over the period, a $10,000 investment would have grown to approximately $15,545. Under the current regime, where investors receive a 50% CGT discount on assets held longer than 12 months, an investor on the top marginal tax rate (currently 45%) would pay tax on half of the $5,545 gain — implying tax payable of roughly $1,248.

What about under the proposed system? Over the same decade, CPI inflation averaged a little above 2.8% per annum. Under the proposed inflation-adjusted approach, the investor’s original $10,000 cost base would rise to approximately $13,250 in nominal terms. Their taxable “real” gain falls to roughly $2,295, producing tax payable of around $1,033.

So, in the case of a relatively ordinary ASX 200 investor over the past decade, you might actually have preferred the proposed system to the current one. I haven’t seen much discussion of that possibility over the past week.

Structure matters

Some investors will pay substantially more tax under the proposed system. Others may pay less. Much depends on the relationship between investment returns and inflation over long periods.

It’s also worth remembering that tax-advantaged avenues for long-term investors still exist. Relatively-speaking, their advantages have just become even more valuable.

The proposed changes do not apply to superannuation structures, including Self Managed Super Funds. The ability to compound investment returns within a concessional tax environment still matters enormously, especially over multi-decade horizons. The structure through which we invest will become even more important if these CGT changes proceed. Before someone points out that the government will one day change super rules too, it is a risk and concern I share.

None of this is to say I support higher taxes. I don’t, particularly in an environment of entrenched government waste. Nor do I think Australia should discourage entrepreneurial risk-taking. We need more ambitious business builders and more investors willing to back them, and this regime is likely, ultimately, to produce fewer of both.

For investors generating good-to-exceptional long-term returns, the changes will hurt. For more conservative or unlucky investors, the impact will be far smaller than many fear, and in many cases beneficial.

Either way, my broader gut feel remains unchanged: Australia has more of a spending problem than a revenue problem. There’s so much low hanging fruit on the cost side, and a complete unwillingness to go after it. It would be nice to see governments confront that reality head on rather than increasingly lean on investors to solve the problems of their own making. In that respect, the frustration expressed over the past week is entirely understandable.

The same AI Narrative, Very Different Software Businesses

The AI sell-off in software has been swift and broad. Investors are asking whether software can now be built more cheaply, whether customers will need fewer licences, and whether margins will be squeezed as companies race to embed AI into their products.

Those are fair questions. But the market’s response has been far less thoughtful than the questions themselves. Software has been sold as a category, as though every business faces the same threat at the same speed.

Australia: switching costs are real

Bravura (ASX: BVS) is a good example. Its software sits at the core of wealth managers and super funds, supporting functions where downtime and errors are not acceptable.

AI may make it easier to build competing products. That does not make it easy to replace a system that is embedded in a client’s operations, tied into multiple workflows, and costly to move away from. In these cases, the key question is not whether the software can be rebuilt, it is whether customers will actually switch.

The UK: low-cost, mission-critical software looks safer

Sage (LSE: SGE), a UK-listed accounting software provider, highlights a different kind of resilience. Its software sits at the centre of payroll, tax and reporting, yet costs little relative to the value it delivers. That makes it highly sticky.

If a product is both important and inexpensive, customers have less reason to take the risk of changing providers. That does not make these businesses immune, but it does make disruption slower than current market pricing seems to assume.

Japan: different fundamentals, same sell-off

Japan stands out because many of its software businesses are still earlier in the digitisation cycle. Customers are still shifting onto modern systems, growth remains strong, and earnings are often cleaner than in the US, with less reliance on stock-based compensation and, in many cases, stronger cash positions.

Despite that, these stocks have been sold off with the rest of global software. That seems too simplistic. In a market where the AI risk is less immediate and the structural growth story is still intact, the sell-off, from a Forager perspective, looks more like a spillover from global fear than a reflection of deteriorating fundamentals.

What matters now

The point is not that AI will not matter. It will. But its impact will vary widely across the sector. For Forager, the framework is simple: how important is the product, how embedded is it in customer workflows, and how hard is it to replace?

If the market is calling this judgment day for SaaS, the real question is which businesses will make it through the trial.

To hear the full discussion, tune in to the full Stocks Neat podcast episode.

Explore previous episodes here. We’d love your feedback. If you like what you’re hearing (and what we’re drinking), be sure to follow and subscribe.

You can listen to Stocks Neat on:

Spotify

Apple

Buzzsprout

YouTube

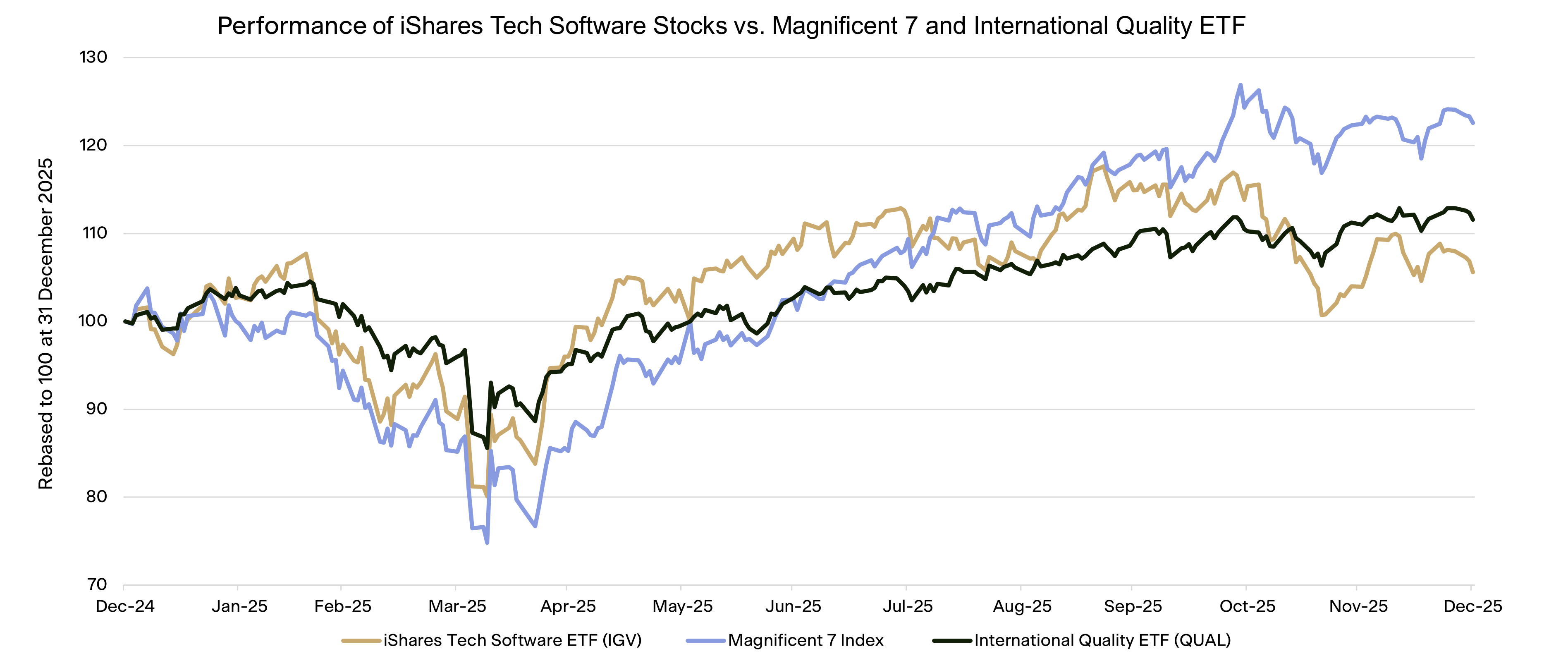

A large part of the software sector deserved its correction.

At the peak in late 2025, many software businesses were extremely optimistically valued. Businesses were ranked using revenue growth alone, often with limited regard for profitability. Where profitability was contemplated, it usually ignored one of the largest expense items for these companies - the prodigious amount of shares issued to staff as compensation each year. The prevailing view was that software economics were structurally superior and largely insulated from disruption. That proved too optimistic.

Now the narrative has shifted sharply in the opposite direction. So much so that the market reaction over the past six months is being dubbed the Saaspocolypse.

Source: Bloomberg

The financial press is increasingly populated with examples of companies reducing software spend by building internal tools. Developers are demonstrating how quickly functional alternatives to established products can be assembled using AI coding agents. There is a growing view that artificial intelligence will, at best, compress margins for many incumbent products and, at worst, disrupt them the way the internet disrupted the newspaper industry.

It will come as no surprise that Forager is sharpening the pencils and has already added a couple of investments to both portfolios. Pessimism is where we thrive.

Working out whether the pessimism is undue or warranted is the hard part. But without it you don’t get great investment bargains.

The key is not to argue that the risks are misplaced. Many are real and will play out. The opportunity lies in identifying the subset of businesses where those risks are either overstated or already reflected in price.

At Forager, we are focused on four characteristics when assessing software opportunities in this environment.

1. High value, low cost

The first is software that is deeply embedded in customer workflows, yet represents a small proportion of total spend.

Accounting platforms such as Xero (ASX:XRO), MYOB and Sage (LSE:SGE) are clear examples. These products typically cost small businesses tens of dollars per month and sit at the centre of financial operations - handling invoicing, payroll, compliance and reporting.

The economic trade-off for customers is straightforward. The absolute cost is low, while the operational importance is high. Replacing these systems introduces risk and disruption for limited financial benefit.

This dynamic is reflected in the underlying economics. Xero has historically delivered strong revenue growth with gross margins above 80% and low churn. Sage, which we have recently added to the Forager International Shares Fund, serves more than 6 million customers globally and generates consistent free cash flow with operating margins above 20%.

Where software is inexpensive, mission-critical and priced for business size rather than number of users, pricing pressure tends to be limited, even as development costs fall.

2. Structural switching costs

The second characteristic is high switching costs.

Software rarely operates in isolation. Over time, it becomes integrated across multiple systems, accumulates data and shapes internal processes. The cost of replacement is therefore not simply the price of a competing product, but the time, expense and operational risk associated with transition.

Bravura Solutions (ASX:BVS) illustrates this dynamic. Its software underpins core functions for wealth managers and super funds - industries with complex regulatory requirements and low tolerance for operational failure. System replacement can take years and involve significant cost.

In this context, the ease of building new software is less relevant than the difficulty of displacing existing systems. Customer inertia, supported by genuine switching costs, remains a meaningful source of durability.

3. Moats beyond software

A third area of focus is businesses where the competitive advantage does not reside in the software itself.

CAR Group (ASX:CAR) provides a clear example. The company’s current market capitalisation is north of $8bn, even after a significant share price retraction. Even if the project were run by the Australian Bureau of Meteorology, even in the days before AI coding, you could replicate carsales.com.au for a few tens of millions. The value is clearly not in the cost of the code. Carsales value instead lies in its position within the automotive ecosystem - connecting a large audience of buyers with a broad base of dealers and private sellers.

This network effect has been built over decades and is reinforced by scale. High levels of traffic attract listings, and listings attract further traffic.

Auto Trader (LSE:AUTO) in the UK demonstrates the same characteristics, generating pre-tax profit margins above 60% in a business where the technical barrier to entry is relatively modest.

These advantages are not immutable. They depend on sustained user engagement and relevance. The eyeballs can potentially transition to AI models, or AI agents can handle more of the looking. But they are not easily or quickly eroded by incremental improvements in software development capability.

4. Value, the sooner the better

It’s our conclusion that the stockmarket Saaspocolypse is unlikely to be an industry wide operational Saaspocolypse. Some businesses will undoubtedly suffer. Some will be beneficiaries of the AI tools now available. That doesn’t make it as simple as buying the survivors.

Even after a significant de-rating, parts of the sector remain far from cheap. And the excessive stock based compensation practices don’t seem to be abating (we have seen some companies increase the amount of shares they are issuing to compensate staff for a lower share price).

We are looking for stocks that are cheap. And the more of the value we get back in the near term, the better.

Bond investors use a concept called duration to assess interest rate sensitivity of bonds. It represents a weighted average life of a bond’s cash flows (so a 30-year bond has a much higher duration than a 2-year bond). If interest rates go up, those longer dated cash flows are worth less in today’s dollars.

The same concept applies to the stock market, which is why you see “growth” assets generally underperform in a rising interest rate environment - their value is dependent on cash flows generated in the distant future. It also applies to their operational risk.

Businesses priced on long-duration assumptions require a high degree of confidence in their ability to sustain growth and competitive positioning over extended periods.

That confidence is harder to justify in a rapidly evolving technological environment.

By contrast, companies that generate meaningful cash flow today and are capable of returning a substantial proportion of their market value within the next decade offer a more balanced risk profile.

Sage and Auto Trader are examples where, based on current earnings and growth expectations, a significant portion of today’s valuation could be returned to shareholders through free cash flow over a 10-year period. This reduces reliance on long-term forecasts and limits exposure to distant disruption scenarios.

The Forager investment thesis

Forager’s International Shares Fund already had a significant investment in Japanese software companies. They continue to grow rapidly, are highly profitable and don’t have the excessive stock based compensation practices of their US cousins. That hasn’t stopped their share prices getting whacked over the past few months, making topping up what we already own the first way we are taking advantage of the opportunity.

Outside Japan, we have added a few undervalued UK and Australian stocks to both portfolios and have the analysis framework in place for more. The shift in the software narrative from "structural superiority" to "imminent disruption" has already created some attractive investment opportunities. Lower prices and an increased focus on shareholder returns would provide the confidence to add more.

If you are interested in finding out more about opportunities the Forager investment team are finding in the Saaspocalypse, subscribe to our investing community

What does a good market hide? Quite a lot. When capital is easy to access and asset prices keep rising, weak businesses can look far stronger than they really are. But when conditions tighten, those illusions tend not to last.

Leverage is the killer

That was one of the clearest takeaways from the latest “Stocks Neat” podcast, where Forager’s CIO, Steve Johnson, sat down for a chat with Julian Biggins: in the end, businesses are rarely killed by a lack of ambition. More often, they are killed by fragility. In his words, “leverage is the killer.” Reflecting on distressed property situations after the Global Financial Crisis (GFC), Biggins noted that the underlying assets were often not worthless at all. The real problem was that the owners had too much debt, could not hold on, and were forced to sell at the worst possible time.

That idea extends beyond property. Across markets, the difference between a good investment and a bad one is often not the asset itself, but the structure around it. A decent asset with too much leverage can become disastrous. An average asset, owned conservatively and managed well, can survive long enough to become a good investment.

Looking past the label

A second lesson from the discussion was that investors should care less about labels and more about what actually sits underneath them. Julian and Steve made the point that “private credit” is not one thing, just as “equities” is not one thing. Within any asset class, there is a wide range of risk. One example Biggins used was mezzanine lending in residential development. It may offer higher returns on paper, but it sits in a far more vulnerable position in the capital stack. If something goes wrong, that layer can be wiped out very quickly, even while the senior lender remains protected.

This is a useful reminder at a time when products are often sold on headline yield or broad category labels. A return number for that broad category on its own says very little. What matters is the assumptions behind it, where you sit in the structure, and how much has to go wrong before your capital is at risk. As Julian put it, detail matters.

Cash flow is king

The same scepticism applies in property. The distinction between an asset that looks attractive on surface metrics and one that actually produces durable cash flow is important. Julian’s point was blunt: “cash flow is king.” Cap rates, accounting yields, and headline rents can all flatter an asset if you do not properly account for incentives, maintenance capex, leasing costs, and the operational effort required to keep income flowing.

His examples reinforced the point . A long-leased Bunnings warehouse can behave almost like a bond, with some inflation protection. A shopping centre, by contrast, is a deeply operational asset where small details - traffic flow, catchment access, tenant mix and layout - can materially change outcomes.

That leads to another theme: the best investors are usually not the ones chasing everything. They are the ones who know exactly where they have an edge. Julian returned several times to the idea that “you just can’t hunt everything.” In competitive markets, breadth is often overrated. Deep capability, local knowledge, and operational control matter more.

Why Tailwinds Matter

There was also a useful strategic lesson in the conversation about tailwinds. Julian noted that even a bright idea can struggle if it is fighting the tide. In investing, it is rarely enough to be directionally right about a business or an asset; it helps enormously if the broader environment is working with you rather than against you. He pointed, for example, to the way tighter bank capital rules and a more cautious approach to commercial real estate lending have opened the door for private credit providers to step into parts of the market banks once dominated.

But even here, the deeper lesson was not “find a tailwind and buy anything.” It was that good businesses build resilience so that no single product, person, or funding source can sink them. Julian described the importance of diversification - not in abstract portfolio terms, but more simply: making sure “no one thing can kill you.” That is as true for portfolios as it is for companies.

In the end, the conversation kept coming back to the same principle: endurance matters more than excitement. You need to invest where you have expertise, avoid being overextended, and stay in the game long enough for the cycle to turn in your favour.

MA Financial is an interesting example of that endurance mindset in practice. Its growth and success have been shaped by the idea that resilience matters more than flash. As Julian puts it, “You don’t need to win in everything. You just need to pick a few that you’re very good at and go through the cycle.” That thinking is reflected in MA’s shift away from the volatility of traditional investment banking and toward more recurring, defensive earnings streams such as asset management, private credit, and lending.

If there is a lesson here, it is not to chase whatever looks strongest in easy times. It is to ask a harder question: what is built to last when conditions turn? That may be a less exciting way to think about investing, but it is often the wiser one. In the end, endurance is not separate from success. It is what makes it possible.

To hear the full discussion with Julian, tune in to the full Stocks Neat podcast episode.

Explore previous episodes here. We’d love your feedback. If you like what you’re hearing (and what we’re drinking), be sure to follow and subscribe.

You can listen to Stocks Neat on:

Spotify

Apple

Buzzsprout

YouTube

After months of headlines declaring that artificial intelligence (AI) would dismantle the software-as-a-service (SaaS) model, updates from several high-quality local software companies this week told a different story. Rather than collapsing under the weight of AI disruption, parts of the sector delivered accelerating growth and upgraded guidance.

TechnologyOne (ASX:TNE), a provider of software to government and education organisations in Australia and the UK, upgraded guidance for profit before tax growth to 18-20%. While Hansen (ASX:HSN), a global software provider to utilities and telco companies, delivered 16% recurring revenue growth and confirmed expected growth and margin over the next few years. Investment platform Netwealth (ASX:NWL) delivered better flows and a solid profit result. Each of the stocks duly rallied.

Given how front of mind it has been for investors, each also explained management’s view on whether AI is a friend or foe.

The existential fear is straightforward. AI is dramatically reducing the cost of developing software. Clients will vibe-code their own solutions for next to nothing. And AI native competitors will proliferate.

TechnologyOne’s response is that resilience depends on the type of software provided. It operates mission-critical software systems in highly regulated environments. These need to be unquestioningly reliable, have the highest levels of cyber protection, and are provided to many users and parts of an organisation.

A treasure-trove of data, deep domain expertise, switching costs and outcome-linked pricing are key defences. The company has 38 years of data, 99% client retention, and long-term contracted clients. “Plus”, the company’s agentic AI platform, is embedded across products and modules, operating within each customer’s trusted environment.

Hansen makes a similar case. Its systems are deeply integrated in complex utility and telco organisations, are highly regulated and difficult to replace. They require almost perfect uptime. Understandably customers are highly risk averse. Customer trust has been earned over decades. And AI is already embedded across the product suite, driving some short term power trading decisions, talking to customers and explaining bills.

Netwealth recognises the pace of innovation will increase. Luckily, the business, alongside other challengers like Hub24 (ASX:HUB) and Praemium (ASX:PPS), are no strangers to innovation. These specialist investment platform providers have attracted advisors by offering better systems, and are likely to continue to do so. There is no shortage of opportunities to add new features and improve advisor efficiency. Scale, regulatory moats and data quality are difficult to replicate. Revenue is linked to funds and transactions rather than seats.

Across all three businesses, common themes emerge.

There will be casualties. AI will put genuine pressure on commodity software providers with limited switching costs. But it looks likely to strengthen mission-critical, deeply embedded systems that have data, workflow and compliance advantages.

If trusted providers with sticky software can deliver advanced AI features, sophisticated clients are unlikely to take a chance on new competitors and run the risk of implementation, training and reliability issues.

From defence to offence

For incumbent software providers, AI functionality is not simply a defensive feature. Instead of shrinking revenue pools, AI can expand them.

When AI improves workflow speed, reduces manual processing or enhances decision quality, the value delivered to the client is tangible. Pricing to customers can then rise to capture the added value. For software businesses already deeply integrated into client operations, AI becomes an upsell opportunity rather than a competitive threat.

Then there are the potential cost reductions for software providers. AI-assisted coding, automated testing and faster product configuration shorten development cycles and reduce the number of software engineers required. Customer service chatbots and agentic support systems lower call centre workloads while maintaining service quality. The business can bank the savings or reinvest them elsewhere.

One banking the savings is investment platform operator Praemium. The business announced a major overhaul of its technology division earlier this week, coming on the back of an acquisition of consultancy Technotia announced in December for $7.5m. The restructure targets duplicate IT development, maintenance and infrastructure roles and represents a meaningful reshaping of the company’s cost base.

Headcount in Australia will fall, and a longstanding Armenian software development operation will close by the end of this financial year. In total, headcount will reduce by 28% and run rate cash costs will drop by $9m. The financial implications are material; free cash flow next financial year should improve by roughly 30%. AI was not specifically cited in the announcement, but would have been helpful in making such significant changes.

Perspective in the panic

The nuance has been lost in the sell-off. Late last year Australian technology valuations were at their highest levels since 2021. Having fallen more than 30%, they are now trading at levels last approaching COVID lows.

Source : Bloomberg

The narrative shift has been swift, and markets have rarely been patient in periods of technological change. But narratives change. Over the next year or two we may see investors focus more on the strength of incumbents, and their ability to reduce costs while growing pricing. In that world beaten down software businesses could well be back in vogue.

In the Forager Australian Shares Fund, the pessimism has created opportunity. After exiting both last year, investments in sports technology provider Catapult (ASX:CAT) and financial services software business Bravura (ASX:BVS) have been added back into the portfolio as stock prices fell sharply and valuations became attractive. Both operate highly sticky mission-critical software in specialist verticals where data and knowhow matters, and where AI can improve cost efficiency while improving the product.

SaaS is not dead. Reporting season suggests that high-quality, mission-critical technology businesses are adapting quickly. The Saaspocalypse may well end up being a SaaSvolution as software providers continue to evolve and grow.

If you're interested in joining our investing community, you can do so by filling in the form below:

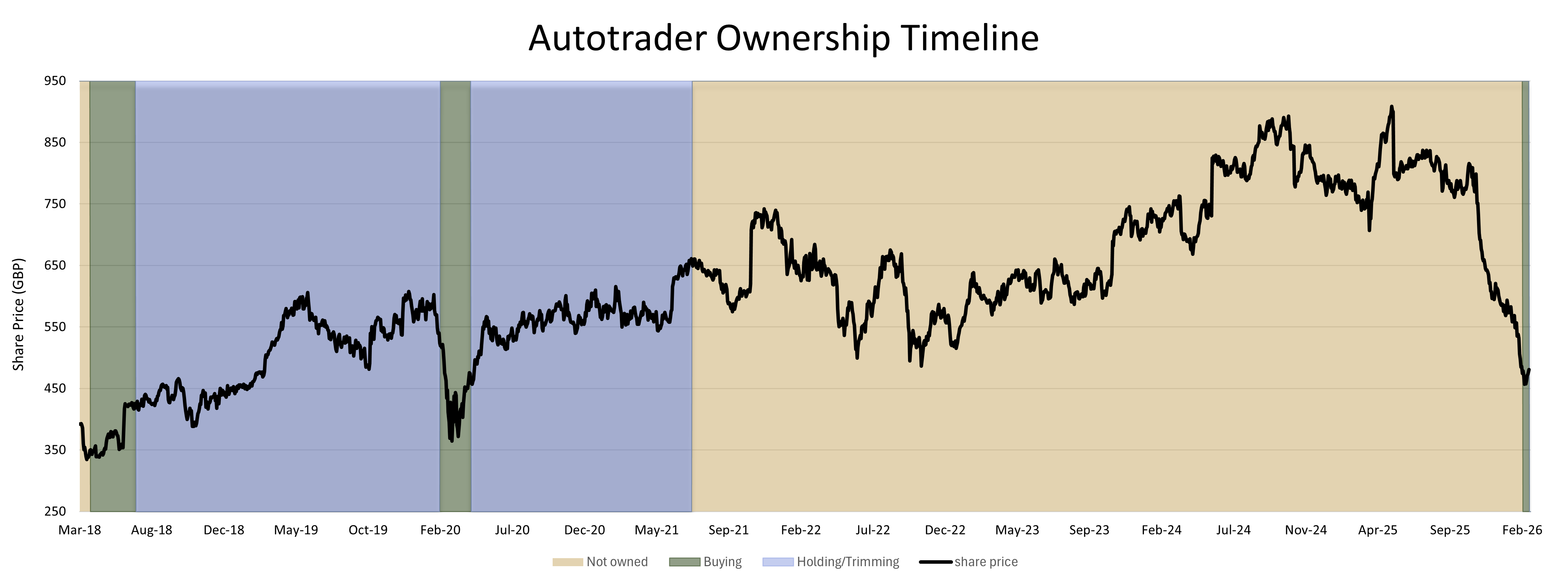

Auto Trader (LON:AUTO) in the UK has been a truly wonderful business for a few decades now. One of the greats.

For every pound in revenue it makes, it only spends 30-35 pence. And that’s after expensing all the research and development necessary to develop new products and offerings to grow the business. Capital expenditure is a rounding error. The remaining 65% is available for the tax office and its owners. The company takes that huge cash flow after tax and returns all of it to shareholders via dividends and buybacks. And yet it grows each year through price increases and new products. Businesses that can grow without having to retain any capital are rare, valuable beasts.

It’s no wonder that investment funds that focus on “great businesses” often own Auto Trader and businesses like it for the long haul. It sells well. “Come and invest in my fund, I buy bombed out crap companies” doesn’t quite have the same ring to it. And “great businesses” is a theme that’s worked well, especially over the past decade or so.

We’re not here to criticise anyone else’s approach. Finding a niche and sticking to it has its advantages. And there are plenty of funds out there that have outperformed Forager’s International Fund over that same past decade or so with an exclusive focus on great businesses like Auto Trader.

But our approach is significantly more flexible.

We love great businesses, sometimes. When we believe that’s where the best risk-adjusted returns can be found, we aim to reflect that conviction with a significant position in the Fund.

We owned Alphabet (owner of the Google Search engine) for many years.

At other times, the portfolio will be skewed towards more complex, less loveable companies, because that’s where we see the most compelling risk-adjusted returns. Norwegian company Bonheur (OB:BONHR) was an example of a successful investment based on an insight or two that few other investors had grasped.

And sometimes the Fund will hold a smattering of highly asymmetric investments where the downside is 100% and the upside many hundreds of percent. Individual investments like that will only ever be small, because they do blow up from time to time. But, when we recognise the best risk-adjusted returns in that space, you can bet the Fund owns some. Nutex Health (NASDAQ:NUTX) being a recent and successful example, and we were loading up on Blancco during its 2017 panic. You get the picture. The ideas in this last category sometimes smell so bad that you wouldn’t want to be in the same room when we explain the investment rationale.

When lower quality or “riskier” businesses turn out to be bad investments, we look like idiots. When we sell a good business on valuation grounds and it soars over the subsequent years, we look like idiots. But the past 12 months have shown that this flexibility has its benefits.

We first bought Auto Trader shares in early 2018 when the market was lowering expectations for the business, at least partly influenced by Brexit pessimism. It got too cheap. We trimmed over 2019 as the price rallied significantly, added again briefly during the Covid-19 panic, trimmed again over the rest of 2020 and were completely out of the stock during 2021.

Source : Bloomberg

Auto Trader is down more than 40% in the past three months.

Add in the recent panic and Forager’s International Fund, which held the stock for a little over three years total, collected more than 100% of the returns that Auto Trader provided to shareholders over the past decade. Significantly more. And we had seven years when those funds could be deployed elsewhere.

It shouldn’t surprise you to read that we’ve acquired a small position in the past few weeks.

Why now? You’ll never guess. We see compelling risk-adjusted return potential.

The market is concerned that Agentic AI poses a threat, either as a direct competitor or by siphoning off the economic pie in a way Google Search never managed to.

One of the reasons Auto Trader has been able to earn such high margins is because it never really needed Google. Customers come directly to its app or website, maybe 20% of traffic arrives via Search, most of it of the free “organic” type. So Auto Trader directly controls the eyeballs of demand, and sells those very valuable eyeballs to car dealers with little friction to outside players like Google.

That contrasts with online retailers like Redbubble and Adore Beauty, where the search engine captures much of the economic surplus. Anything that upsets that virtuous cycle of eyeballs and advertisers is a threat to Auto Trader’s mouth-watering margins. Older investors might remember that those antiques called newspapers were great businesses too until the likes of Auto Trader rocked up.

The risks are real. At today’s price, it’s our view that investors are getting well compensated for them. Auto Trader should be able to embed AI tools in its existing offering and keep those eyeballs coming back. On our numbers, the business will generate its entire current market capitalisation in cash over the next decade. It has been buying back up to 0.1% of its own shares every single day over the past few weeks.

It was the right time to start allocating chips. We’ve bought from some panicked investors, perhaps a fund that only invests in “Great” businesses. Our investment may get bigger. It’s also likely to be joined in the portfolio by other high-quality companies getting hammered for the same reasons. Put simply, when good businesses are under a cloud, it’s time for Forager to get interested.

They won’t all work. This is not an easy pitch to potential clients. Planners and advisors particularly find it hard to recommend us to their clients. We're a source of unknowable risk, not so much the risk of losing money (something all funds face) but not knowing in advance how we might lose them money, which "factor" might do the damage when we get it wrong.

That’s understandable. But it’s the strategy that works for us and our like-minded clients.

If you're interested in joining our investing community, you can do so by filling in the form below:

In 2025, much of the excitement (and much of the return) in global stock markets was concentrated in a relatively small group of large companies. The Forager International Shares Fund finished the 2025 calendar year ahead of the MSCI All Country World Index. Yet most of the Fund’s returns came from companies few investors would recognise and none were considered “AI leaders”. If not from the obvious winners, where did those returns come from? There are three key ways Forager’s International Fund has managed to overcome this headwind within the small-cap space.

Small companies can still ride the trend

Global investment in AI infrastructure accelerated sharply in 2025, with the “Big Four” spenders (Google, Microsoft, Amazon and Meta) increasing their capex spend 62% year-on-year. That spending flowed beyond chipmakers and hyperscalers into data centres, power generation and industrial services. Several Fund investments benefited directly from that surge in capital expenditure, even though they were not labelled as “AI stocks”.

Heating, ventilation and cooling contractor Comfort Systems (NYSE: FIX) saw rising demand as data centre construction increased, with its share price up 120% in 2025. Solar equipment manufacturer Nextpower (NASDAQ: NXT) benefited from the same build-out, supplying infrastructure to energy-intensive computing facilities, and its share price rose 138% over the calendar year.

That distinction mattered. It showed investors did not need to own the most crowded names to benefit from structural change. In a dispersed market, indirect exposure bought at the right price could be just as powerful and often came with far less competition.

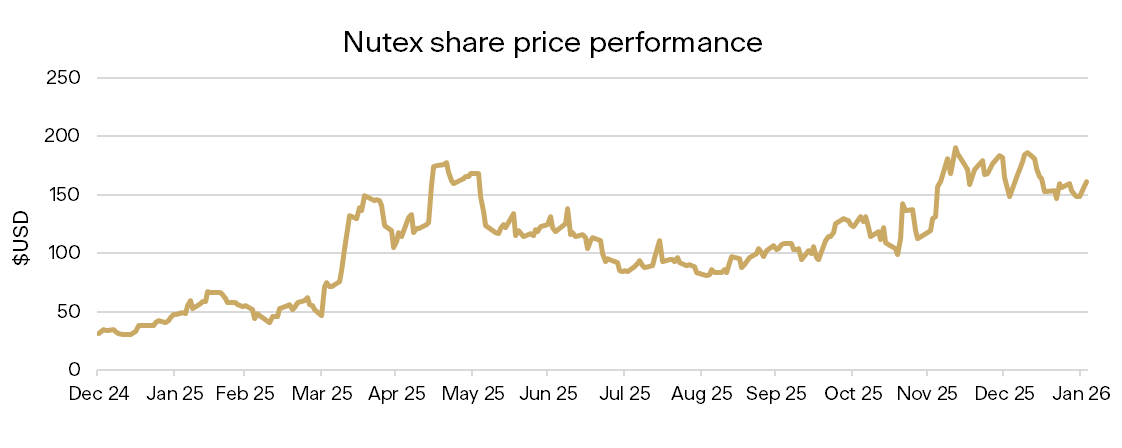

Nutex Health and the value of idiosyncrasy

Nutex Health (NASDAQ: NUTX) reinforced that small idiosyncratic winners can go the opposite way to market trends.

The healthcare sector as a whole struggled for much of the year, with the iShares U.S. Healthcare ETF returning just 12% for the 2025 calendar year. Nutex, however, did not. The stock returned 351% over the year, driven by company-specific execution rather than broader sector momentum. This was not a linear increase; there was plenty of volatility along the way. However, while volatility was elevated, active portfolio management allowed the Fund to benefit from these price swings rather than be hindered by them, resulting in a fivefold increase in the share price since the Fund’s initial purchase.

Zegona: a complex situation that paid off

At the small end of the market, value realisation events can provide big wins in difficult markets. Zegona Communications (LON:ZEG) is one such example.

The Fund invested after Zegona acquired Vodafone Spain, a deal financed with a complicated structure. For many investors, the complexity alone was enough to stay away. For Forager, the complexity was the opportunity.

If Zegona's experienced management team could sell assets and simplify the structure, Zegona's equity would become much more valuable. Over the past six months, Zegona sold its fibre assets, generating €1.8 billion of upfront proceeds. These proceeds fully funded the redemption and cancellation of Vodafone’s preference shares, reducing the ordinary share count by 69%, alongside a shareholder dividend and debt reduction.

As the risks fell away, the market reassessed the share value, sending the price up 130% from initial purchase - a special situation that paid off for shareholders while many large telecommunications companies were struggling.

The bigger picture on small-cap opportunities

For Nutex and Zegona, the common thread was not the sector or the theme. It was the idiosyncratic nature of the situation, where what mattered most was what the company did, not what the market expected.

This kind of investing is often volatile. Evidently so, given the Nutex share price has fallen 35% in 2026. But these examples show winners can be found at the small cap end of the market if you are prepared to do the work and to look where others are not.

The Forager International Fund has generated value for clients beyond the mega-caps that have driven market performance over the past five years. Should those leaders lose momentum, the advantage of the Fund’s differentiated, idiosyncratic approach is likely to become even more evident.

If you haven't already joined our investing community and would like to find out more about idiosyncratic global stock ideas, please fill in the form below:

.png)

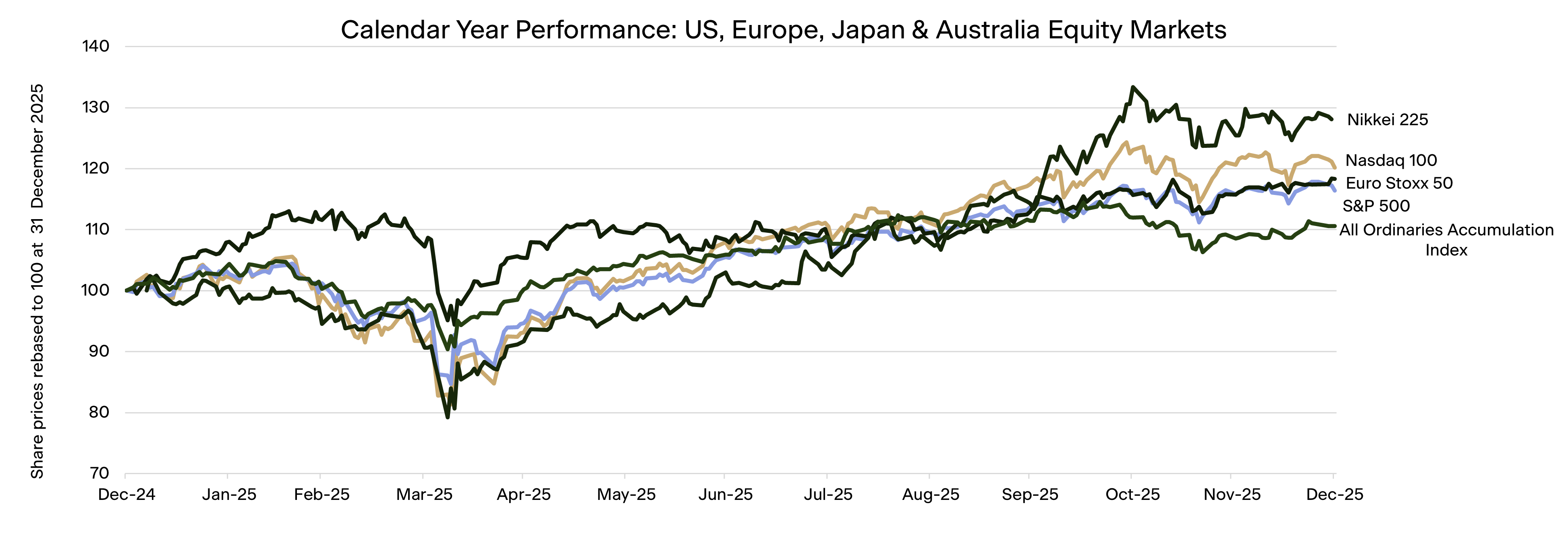

If you look only at the headline index numbers this year, 2025 looks fairly straightforward. The All Ordinaries Accumulation index returned just over 10% for the year and the MSCI World Index approximately 20%, putting both modestly above long-term equity returns of 7-8% per annum. On the surface it looks like a decent, if unspectacular, year. Under the surface, it was far more eventful.

The Australian market was one of the worst performers globally. While the tech-heavy Nasdaq Index (+20%) outperformed the broader S&P 500 (+16%) for the year on the back of big tech and Artificial Intelligence (AI) enthusiasm, it was a strong year for European markets too, particularly those in the south. Italy’s FTSE MIB rose 32%, Spain’s IBEX 35 added 49% and Greece’s ASE Index a whopping 44%.

Source : Bloomberg

Even within markets, dispersion has been the defining feature of the year. The gap between winners and losers has been wide. Abnormally, that has almost been as true at the larger end of the market as the smaller end. Here in Australia, investors in the likes of CSL (ASX:CSL),CBA (ASX:CBA) and James Hardie (ASX:JHX) learned that size doesn’t protect you from things going wrong. In fact, for the first time in a long time, the Small Ordinaries’ almost 25% return trounced the All Ordinaries for the year, with mining stocks, especially gold-related, posting a bumper calendar year (the ASX Small Ordinaries Resources Index was up 70%). Even in the Nasdaq 100, 20 stocks fell more than 10% in 2025.

Dispersion has always been a feature of financial markets. If it didn’t exist, we wouldn’t have a job. As much as balance sheet analysis and stock valuation matter to Forager’s process, a huge component of our excess returns involves finding unpopular stocks that can one day be popular again. Benjamin Graham quoted Horace almost 100 years ago in his seminal value-investing book Security Analysis and the philosophy is relatively unchanged:

“Many shall be restored that now are fallen, and many shall fall that are now in honour.”

What has changed is that the waves of popularity seem more extreme than ever. We’ve written a lot this year about the structural influences increasing the momentum-driven nature of stock markets. Want to bet on European defence stocks? Here’s the Betashares Global Defence ETF for you (ticker ARMR), available via any Australian broker and up a miserly 44% in 2025.

While it can be painful to miss these waves and even worse to get dumped by one, the opportunities for the patient long-term investor are excellent. The unloved can be a source of great ideas, and the payoff even better than expected if the sentiment changes for the better.

Some nice waves in 2025

With concentrated portfolios and small-cap stocks, there will always be a strong idiosyncratic element to Forager’s returns. The most significant contributor to the Forager International Fund’s 15% return in 2025 was US hospital owner Nutex Health (NASDAQ:NUTX). Its share price rose 420% for the year despite the healthcare sector as a whole struggling. Cuscal (ASX:CCL) was the second biggest contributor to the Australian Fund’s returns despite the payments sector globally having a very difficult year.

But we also managed to catch a few of those big waves that defined the year on stock markets. AI companies’ insatiable demand for data centres and power generation led to 120% and 139%respective returns for heating and cooling system installer Comfort Systems (NYSE:FIX)and solar equipment company Nextpower (NASDAQ:NXT) in the International Fund. And a widespread tech rally in the first nine months of the year led to sensational gains for our once-cheap collection of ASX-listed tech stocks like Bravura (ASX:BVS) and Catapult (ASX:CAT). Both of those companies were added to S&P/ASX indices, boosting their returns, and Comfort Systems and CRH were added to the S&P 500.

The net result was very healthy gains for both funds despite large parts of the market (and our portfolios) not “working”.

Past performance is not indicative of future performance and the value of your investments can rise or fall. Performance returns are calculated using exit prices, net of all fees and expenses and assume distributions have been reinvested.

Where to catch a wave in 2026

Looking into the year ahead, the first place to consider is always your local surf break. In 2025, some of our favourite investing sectors became too popular and crowded. As outlined in the September Quarterly Report, we banked profits on the likes of Catapult and Bravura, but they, and many of their peers, are well entrenched on the watchlist. The subsequent three months saw a significant pullback across the whole ASX-listed tech sector. Catapult’s share price fell 40% for the final quarter of 2025 and Bravura was down 27% from its recent high on 10 October. Even market darling Xero (XRO) fell 41% from its highs in June.

Some of them are perceived to be AI losers. The value of software, in a world where anyone can use AI to “vibe code” their way to a new website or app, is significantly diminished. That’s the theory.

It is a theory we are willing to bet against at the right price. Forager is a user of Xero’s product and won’t be vibe coding our accounting software any time soon. Even if we could build an accounting system, software isn’t just about features. Security, backups and constant improvements are at least as important. There is no chance of us taking a risk on any of those in order to save a few thousand dollars a year.

Source : Bloomberg

Many of these stocks had become expensive. Despite the recent falls, the share prices of most are still up meaningfully for the year and still aren’t cheap enough (including Xero). We haven’t deployed much capital into the Australian stocks yet, but are a lot closer than we were just three months ago. In the International Fund, we have added three technology companies that have each halved and worse over the course of 2025 and hope to add a few more. All three can be substantially higher portfolio weights should we get some thesis-confirming evidence over the next few quarters.

“Quality” has its year in the shade

Who wouldn’t want to buy a business with a strong moat, decades of earnings growth behind it and a great management team? Not only does investing in these “quality” businesses sell well, it has worked well for most of the past 15 years. In 2025, it didn’t. Australian investors in favourites like Carsales (ASX:CAR), Resmed (ASX:RMD), Cochlear (ASX:COH) and CSL suffered the same fate as investors in global equivalents like UK property website Rightmove (LON:RMV)and global insulin and weight loss giant Novo Nordisk (CPH:NOVO-B).

Share prices had been growing faster than earnings for many of these companies and the past year showed that the resultant high multiples can be a problem, even for the best of businesses. The result can be years of no returns while the earnings catch up to the share price. Or a significant derating if the earnings and the multiple come into question. Both Novo Nordisk and CSL suffered the latter fate in 2025. So did Fiserv (NASDAQ:FISV), a long-held investment in our International Fund.

We, too, like these quality attributes when we can buy them for an appropriate price. For Forager, they are inputs into our valuations, rather than a standalone investing strategy. We can and do buy lower quality businesses and invest in riskier situations, managing the risks with portfolio management. That flexibility has been helpful this year—some of our lower quality businesses have generated excellent returns—and the flexibility might also help find some quality opportunities at attractive prices in 2026.

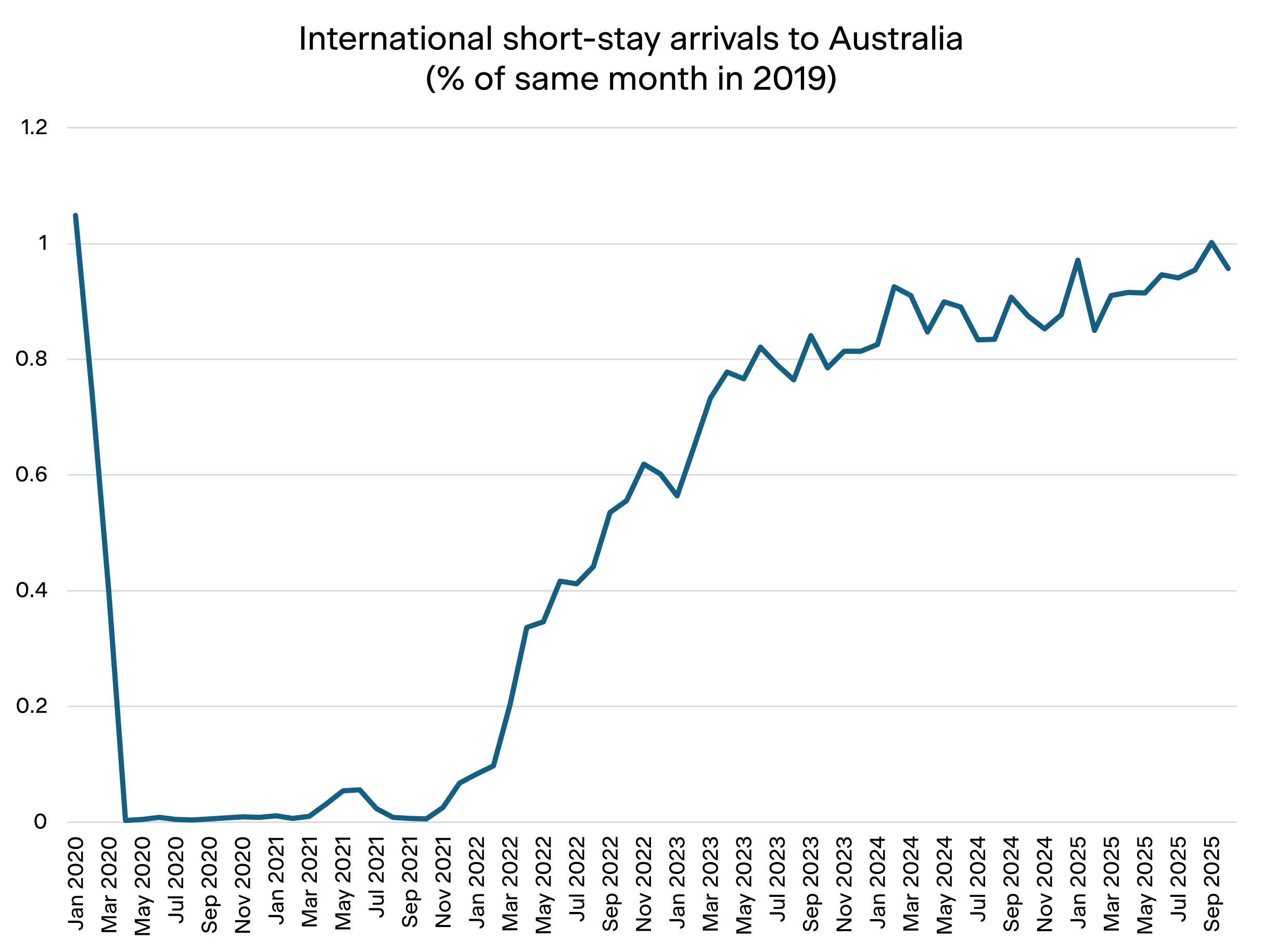

Australian tourism finally recovers?

We’ve been paddling around this beach for four years now, were dumped twice and haven’t caught a wave. But could 2026 be the year Australian tourism finally gets some momentum?

Source: Australian Bureau of Statistics, Overseas Arrivals and Departures, Australia October 2025

There are not many great businesses in the tourism sector. There are exceptions, like global travel booking platform Booking Holdings (NASDAQ:BKNG) and scaled, asset-light hotel operators like Accor (EPA:AC) , but the industry is generally characterised by low barriers to entry and wild swings in demand. Stock prices for our two ASX-listed tourism companies, Experience Co (ASX:EXP) and Tourism Holdings (ASX:THL), remain near 2022 levels.

Yet the environment continues to improve. International arrivals into Australia set post-Covid records in the past three months. Relative to 2019, August, September and October combined saw arrivals hit 97% of the equivalent period in the year prior to Covid. It’s been a longtime coming, but there is no reason the growth should stop there. Travel has historically grown at a multiple of GDP growth and there is still some catching up to do.

Those two stocks are very cheap on anything like recovered earnings. And we have recently added a Spanish hotel booking platform company to the International Fund. Its earnings have already recovered, but it trades at a multiple of just six times those earnings.

Given the amount of suffering in the sector over the past decade, it’s hard to see others getting too excited. Less pessimism would help, though. And who knows? Our mining services investments spent a decade in the wilderness before doubling and more over the past 12months (in Perenti’s (ASX:PRN) case, mostly after we sold it). A travel ETF anyone? ASX code FUN, of course.

An environment that should only get better

Forager will likely get off waves far too early. We may well stay on a few too long. We are going to suffer periods where we miss them altogether and others where we paddle around waiting for a wave for years longer than we initially might expect. But the swells creating good investing conditions aren’t going anywhere. Active equity strategies saw record outflows again in 2025. The running total globally is US$3 trillion out of active and US$6 trillion into passive strategies since 2015*. It has been another year where we saw multiple active managers liquidate their portfolios and shut up shop in Australia. For those of us fortunate enough to have loyal long-term clients and some good results on the board, that’s all a source of opportunity that’s hard to see going away.

*latest data from at https://www.ici.org/research/stats/combined_active_index

This is an excerpt from the upcoming December 2025 quarterly report. If you would like to receive the report to your inbox, please subscribe to our investing community:

The Business of Booze: Can Zero be Diageo's comeback story?

The global alcohol industry has long been considered a steady, defensive corner of the market. But in the latest episode of Stocks Neat, hosts Steve Johnson and Gareth Brown unpack why that assumption has been badly tested in recent years, and what, if anything, might revive the sector.

Drawing on Gareth’s recent trip to London and conversations with global drinks giant Diageo (LON:DGE), the episode explores falling consumption and generational change. Plus the surprising role alcohol-free beer could play in reshaping the industry’s economics.

A sector nursing a hangover

Once prized for its reliability, alcohol has become a difficult place for investors. Diageo’s share price, for example, has more than halved from its 2022 peak. As Gareth explains, Covid accelerated demand for alcohol, but global sales volumes have been falling each year since.

World alcohol volumes have been flat to falling since 2022, with younger generations drinking less, or not at all.“There is a significantly higher percentage of that 18 to 35 bracket that abstain from alcohol,” Gareth notes, as health consciousness and cost of living pressures reshape how younger people socialise. Add to that the rise of substitutes like legalized cannabis in parts of the US, which has particularly hit beer consumption, and it’s clear why markets have soured on what was once seen as a “cash machine” industry.

Premiumisation, pressure, and profitability

Gareth’s argument is that beer used to deliver better returns because it can be made quickly, so breweries can reuse the same production assets and working capital more often. But the rise of craft beer and easier access to distribution has increased competition and pricing pressure, which has eaten into beer’s old advantage.

Furthermore as Steve puts it, the old moat of mass advertising and sponsorships is largely gone. Today, celebrity-backed spirits and boutique brewers can reach consumers directly, forcing incumbents into a costly game of catch-up.

The Guinness Zero surprise

One of the most intriguing insights from Gareth’s London trip is the resurgence of Guinness, powered in part by Guinness Zero. In UK pubs, Guinness now appears to dominate taps, and alcohol-free Guinness reportedly accounts for a significant share of sales.

During the episode, Steve and Gareth even conduct a blind taste test between regular Guinness and Guinness Zero. The result? Both could tell the difference, but only just.

“It’s easier to make a complex zero-alcohol beer than a simple one,” Gareth explains, suggesting why brands like Guinness may have an edge as consumers cut back without fully opting out. Crucially, Guinness Zero sells at similar prices to its alcoholic counterpart, without excise taxes, creating potentially attractive economics for producers.

Key moments in the episode

- [00:39] Why Stocks Neat is tackling the “business of booze” now

- [03:17] Gareth on meeting Diageo and why big incumbents still matter

- [05:26] Global alcohol consumption trends—and why volumes may never recover

- [08:13] Younger generations, abstinence, and the cost-of-living squeeze

- [12:23] Cannabis as a substitute: why beer has been hit hardest

- [15:55] Beer vs wine economics and lessons from past industry mistakes

- [21:55] Guinness, alcohol-free beer, and a blind taste test surprise

Watching, not rushing

The episode ends on a cautious note. While the sector still generates enormous cash, its future depends on how younger consumers behave if economic pressures ease and whether management teams resist the urge to chase growth through expensive acquisitions.

For now, Steve and Gareth remain watchful rather than bullish. But as this discussion shows, even a troubled industry can offer insights and even opportunities if you look closely enough.

Listen to the full episode of Stocks Neat for the complete conversation and taste test.

Explore previous episodes here. We’d love your feedback. If you like what you’re hearing (and what we’re drinking), be sure to follow and subscribe.

You can listen to Stocks Neat on:

Spotify

Apple

Buzzsprout

YouTube

In the September 2025 Quarterly Report Chief Investment Officer, Steve Johnson, asked a simple question. “With optimism spreading, should our concern levels be rising?” It captured the mood in the team at the time. When confidence becomes widespread, caution becomes more important.

Here at Forager, the investment team has been proactively and successfully preparing both Fund portfolios for potential market volatility by raising cash and shifting toward defensive businesses. This puts the Funds in a position to capitalise on opportunities when they emerge. Might we get our chance soon?

Preparing Our Portfolios for More Turbulent Markets

Long before any volatility appears on screens, the investment team is already doing the work behind the scenes. That preparation has been underway for some time. We have been trimming or exiting positions that have run too far and taking profits when prices no longer reflect long-term value.

Two very clear examples come from the Forager Australian Shares Fund. Catapult (CAT) and Bravura (BVS) were both strong contributors to returns this year. We sold out of both when their valuations became stretched. Not because the businesses had deteriorated, but because the prices no longer made sense for patient, long-term investors.

We have also been lifting cash levels in both portfolios so we have the ability to act when opportunities return. Alongside that, we have tilted both portfolios towards some steadier, more defensive businesses that tend to hold up well when things get bumpy.

This is not about forecasting. It is about being ready. Our approach relies on a disciplined process. When good businesses become too expensive, we step aside. When they fall back to sensible prices, as some are beginning to do, we want to be in a position to own them again. Flexibility is a key part of our investing philosophy and holding a little more cash gives us room to move when the right chances appear.

Not all share price falls are created equal

Although we are nowhere near peak pessimism, there have been enough recent moves to suggest a shift in tone.

Some companies fall because their underlying businesses are simply not good enough. Weak balance sheets, poor strategic decisions or ineffective management eventually show up in the numbers. When these prices fall, they often stay low. We aim to avoid these businesses altogether.

Then there are the much better businesses. The ones with strong fundamentals, loyal customers and the ability to grow for many years. Prices for these companies can fall too, usually for reasons that have little to do with the underlying business.

Sometimes they have simply run too far ahead of their actual earnings. Sometimes short-term sentiment takes over. The underlying business remains sound but the share price takes a hit.

Since our exits, share prices for both Catapult and Bravura have fallen around 25 to 30%. They have plenty of friends at the moment. Life360 (360) has been on a similar journey. While we owned this company for a while back in 2020, we missed its most recent ascent. The business has grown and improved and we would love to own it again, at the right price.

Internationally, we are seeing a similar pattern. Index returns look healthy on the surface, yet many individual companies have been hit hard. The headline numbers are being propped up by a small group of winners, particularly in the Nasdaq 100, where 15% of companies are trading at levels more than 50% below their all-time highs.

This is exactly the sort of cycle we hope for. Strong businesses become expensive, we exit, then a pullback gives us a fresh look.

Get ready, get excited

Even after their recent pullbacks, share prices for Catapult, Bravura and Life360 remain well ahead this calendar year, up 36%, 15% and 75% respectively. Whilst there have been some cracks emerging, this is nowhere near peak pessimism. What matters is that we are ready if conditions do become more challenging. Let’s hope that these cracks become craters so we can put that cash to work.

If you’ve followed the Forager Australian Shares Fund for a while, you might have noticed a theme: a surprising number of our investments end up acquired by another company. From small technology firms to niche industrials, our portfolio has been a fertile hunting ground for private equity firms and larger companies looking for attractive acquisitions on the ASX.

The prevalence of takeovers in the portfolio is not by design - at least, not entirely. And they haven’t all been great investments. On more than a few occasions - Bigtincan and Whispir come to mind - an eventual takeover was simply relieving us of our misery. Even for the losers, strategic appeal can provide important downside protection.

In June we wrote about five Australian small cap takeover candidates to complement the three portfolio investments already under takeover at the time. Mining technology business RPMGlobal (RUL) has been the first of these to receive a formal bid. At the time we wrote:

“The potential for a takeover at a healthy premium is a nice kicker when the fundamentals are strong, the valuation is attractive, and the assets have strategic value. With our focus on the unloved and underappreciated, we think we hold a few of those. Let’s see if would-be acquirers agree.”

In the case of RPMGlobal, global mining equipment behemoth Caterpillar Inc (NYSE:CAT) very much agreed. Caterpillar has bid $5.00 per share in a deal which values RPMGlobal at over $1.1bn, or nearly 15 times recurring software revenue. The Forager Australian Shares Fund first bought shares at $0.77 six years ago.

Today’s piece is about how to find the next RPMGlobal.

Buying it cheap

The first ingredient of a highly successful takeover candidate is to buy it cheap to start with. When Forager first invested in 2019, RPMGlobal was an underappreciated business with world-class mining software, recurring revenue from a growing global client base and a management team intent on reshaping the company.

A transition from multi-year software licences to annual recurring software subscriptions was a handbrake to revenue growth and profitability. The value in the company was hidden. Once the subscription transition was complete, revenue growth and free cashflow would be plain to see.

Buy a business you want to own anyway

In the last three years subscription software revenue more than doubled. Very few clients turned the software off. And existing clients were spending more on their software every year.

Source: Bloomberg

While we waited, RPMGlobal grew, generated cashflow and bought back its own shares. The longer it took, the more we stood to make when a takeover finally arrived.

If you are happy owning the business anyway, you are far more likely to end up with an outstanding result on takeover.

The right management team

RPMGlobal’s management executed superbly during our period of ownership. All with one eye on an eventual sale, they simplified the business, sold non-core divisions, and invested heavily in software development. The transition to a subscription-based model built predictable, high-margin revenue streams and demonstrated the scalability of the product suite.

By the time Caterpillar came knocking, RPMGlobal had become a global leader in mine scheduling, mining equipment management and mine financial software. This is exactly the kind of asset a company like Caterpillar could integrate into its digital ecosystem. Not many CEOs want to work themselves out of a job, but Richard Mathews had prior form and enough shares to make the hard work worthwhile.

Strategic value

The final and most important ingredient is for the business to be worth more to someone else than it will ever be worth on the stockmarket. For Caterpillar, the acquisition strengthens its position in mining technology and provides access to RPMGlobal’s best-in-class software and deep customer relationships across the mining industry.

And for RPMGlobal shareholders, being listed is expensive. The board, listing costs and corporate overheads chewed up roughly two thirds of RPM’s operating profits in the 2025 financial year. Not only does Caterpillar get a strategic asset, it won’t incur many of those costs, making the acquisition price a lot more palatable.

For shareholders, the $5.00 per share offer represents a significant premium and an excellent crystallisation of value. For Caterpillar, it makes sense too. The best deals often do.

If you'd like to find out more about the Forager Australian Shares Fund, you can do so here.

DISCLAIMER: The Trust Company (RE Services) Limited (ABN 45 003 278 831, AFSL No: 235150) is the responsible entity and the issuer of the Forager Australian Shares Fund (ARSN No: 139 641 491). You should consider the product disclosure statement (PDS), prior to making any investment decisions. The PDS and target market determination (TMD) can be obtained here. General advice only and does not take into account the objectives, financial situation or needs of investors. Past performance is not indicative of future performance and the value of your investment can rise or fall.

High Performance In and Out of the Pool

From Olympic gold to the ASX 200, Generation Development Group CEO Grant Hackett joins Steve Johnson for a special episode of Stocks Neat.

They discuss Grant’s journey from elite sport to business leadership, the importance of purpose beyond success, and how lessons from swimming translate into building a $3 billion company.

As Grant shares: “You’re retired to something, not from something.”

The conversation also dives into Generation Development Group’s core businesses, from investment bonds and annuities to Lonsec and the rise of managed accounts, and how the company is navigating growth, regulation, and leadership under pressure.

Make sure to stick around to the end of the podcast, for a candid talk between Steve and Grant.

Explore previous episodes here. We’d love your feedback. If you like what you’re hearing (and what we’re drinking), be sure to follow and subscribe – we’re doing this every quarter.

You can listen on:

Spotify

Apple

Buzzsprout

YouTube

In the latest Stocks Neat episode, Steve Johnson, Gareth Brown and Isabella Foley dive into Japan’s corporate transformation — from shareholder returns and buybacks to digitisation and the demographic shifts reshaping opportunities.

With Japan now a significant part of the international portfolio, the team shares where they’re finding value and why some of the most interesting ideas are hiding in plain sight.

“It’s been like a snowball that’s been pushing across a flat surface for a long period of time. It’s finally started to gather some momentum.” – Steve Johnson

Explore previous episodes here. We’d love your feedback. If you like what you’re hearing (and what we’re drinking), be sure to follow and subscribe – we’re doing this every quarter.

You can listen on:

Spotify

Apple

Buzzsprout

YouTube

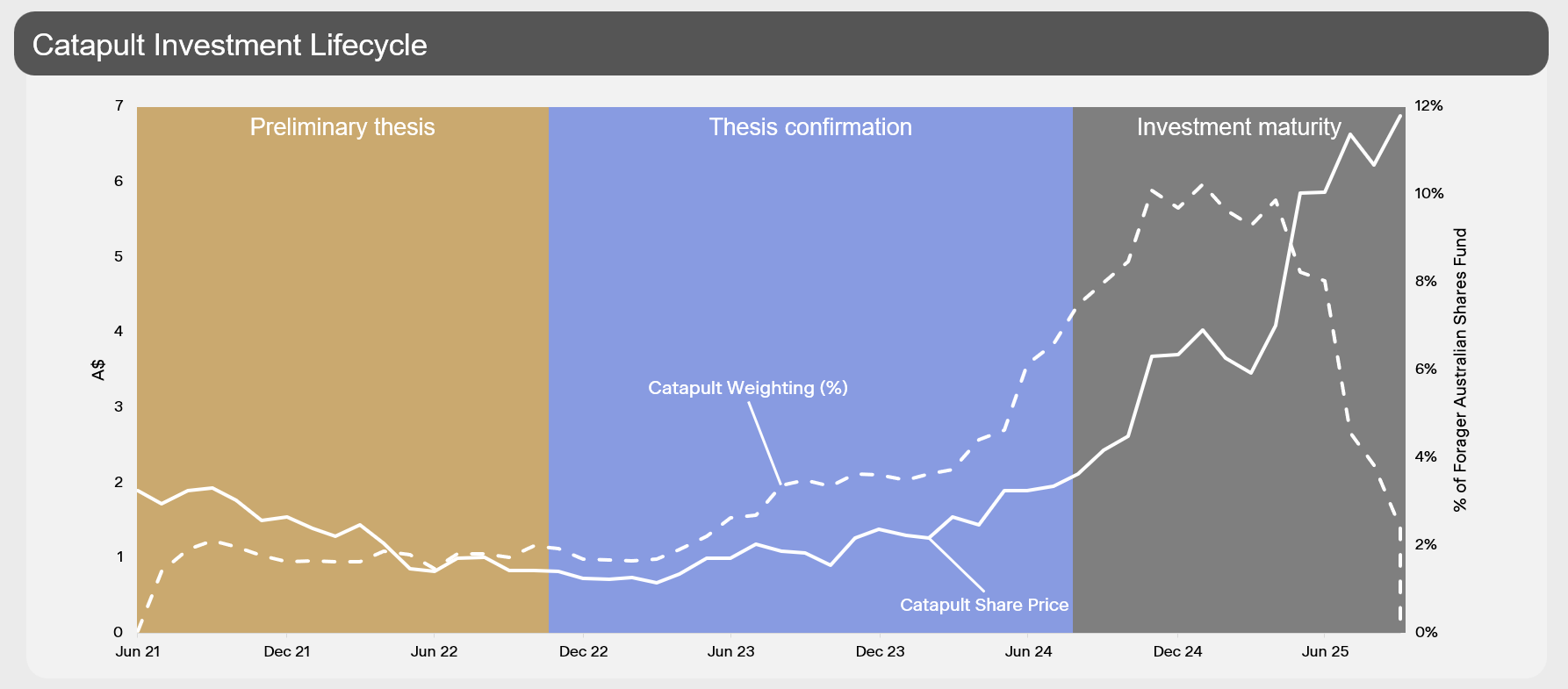

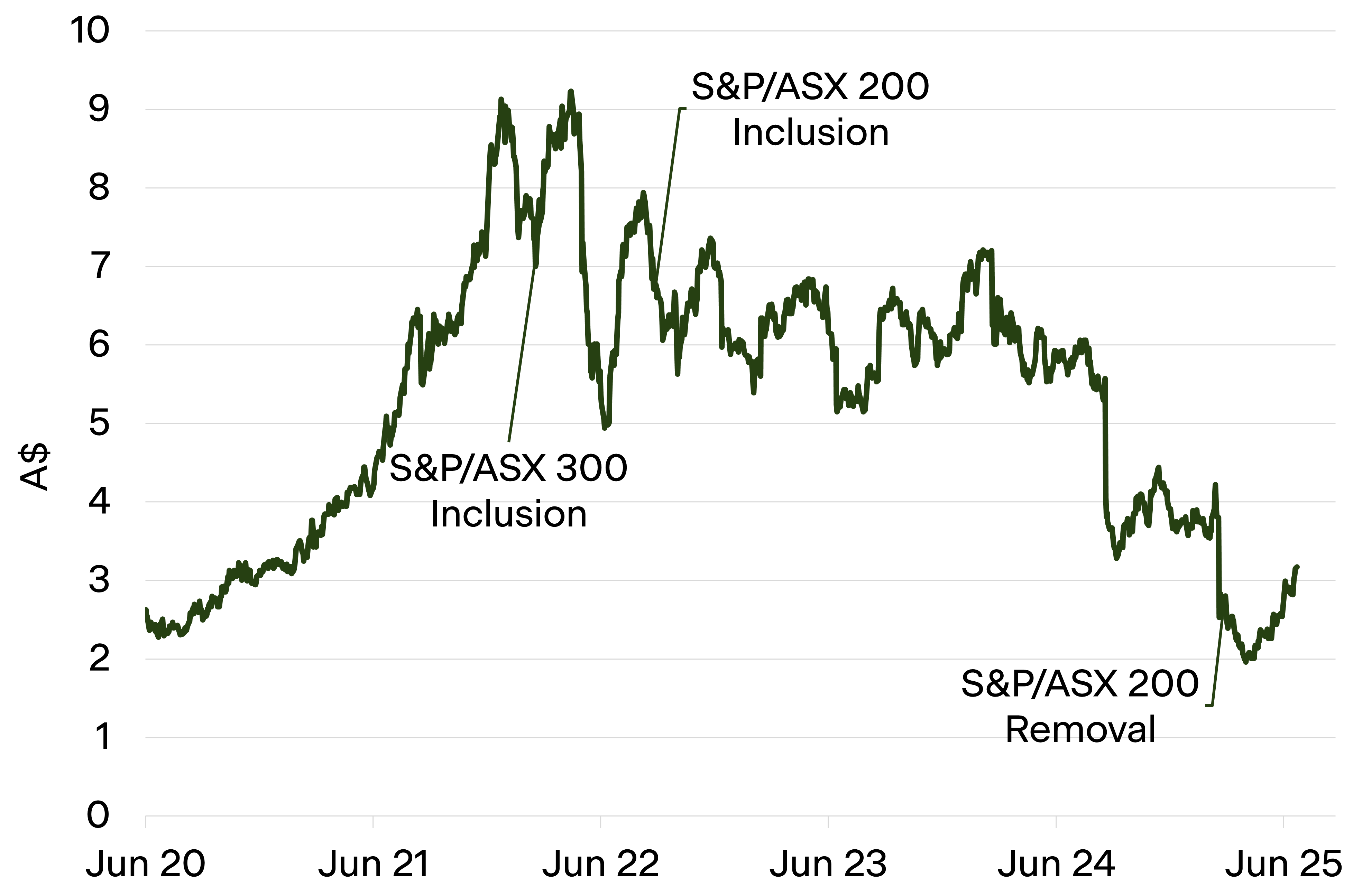

Investing in unloved and underappreciated stocks is rarely comfortable. It often means doubting what other investors believe and backing ideas others dismiss. Our journey with Catapult Sports (CAT) was an exercise in patience and conviction that has now rewarded us handsomely. Yet this investment has now come to an end - the Fund sold the last of its shares in Catapult this week.

Forager’s first purchase of Catapult shares was June 2021 at $1.90 per share. Almost two years later, in April 2023, we were adding to the Fund’s investment between $0.70 and $0.80. With the share price north of $6, it has been a wonderful investment for Forager investors and anyone who played along.

It’s not the first investment on which we have made those sorts of returns. Gentrack (GTK) and RPMGlobal (RUL) have been similar-sized winners in recent years. Yet Catapult is the stock where we best applied 16 years of lessons to truly optimise a successful investment:

1. Low Initial weighting. The initial weighting was less than 2% for several years. This allowed us to more easily cut the investment with limited damage had our contrarian view been proven wrong.

2. Adding on strength. We added to that low initial weighting on good news, even after the price had risen. While paying $1.50 a share after seeing $0.70 isn't easy, building confidence in a thesis allows for a crucial counter to the risk-minimisation of a low initial weight. At its peak, Catapult was more than 10% of the Fund.

3. Capturing the upside. We held a higher-than-usual portfolio weighting to capture the maximum upside as Catapult moved from a relatively unknown stock to an ASX300 member with major investment bank research coverage.

4. Winding back. And yet we are valuation-driven investors. There is a point when higher stock prices create a valuation at which future returns no longer meet our minimum thresholds. This is where we have arrived with Catapult.

And so our journey has come to an end.

In the weeks after recording Livewire’s innovation episode of Buy Hold Sell, Catapult was a surprise replacement for Gold Road in the ASX200 index. That sent the share price up another dollar, leaving the company sporting a market capitalisation in excess of $2bn. This price-agnostic index buying was a good opportunity to exit the last of our holding.

It still has the same bright future we hoped for when making our first investment four years ago. But today’s valuation reflects a bright future and a bit more. We have barely changed our numbers over the four-year holding period, meaning time and sentiment alone have driven the share price to its current level.