After decades of frustrating capital allocation and entrenched complacency, Japanese corporate governance is finally undergoing meaningful change, and it’s starting to show up in investor returns.

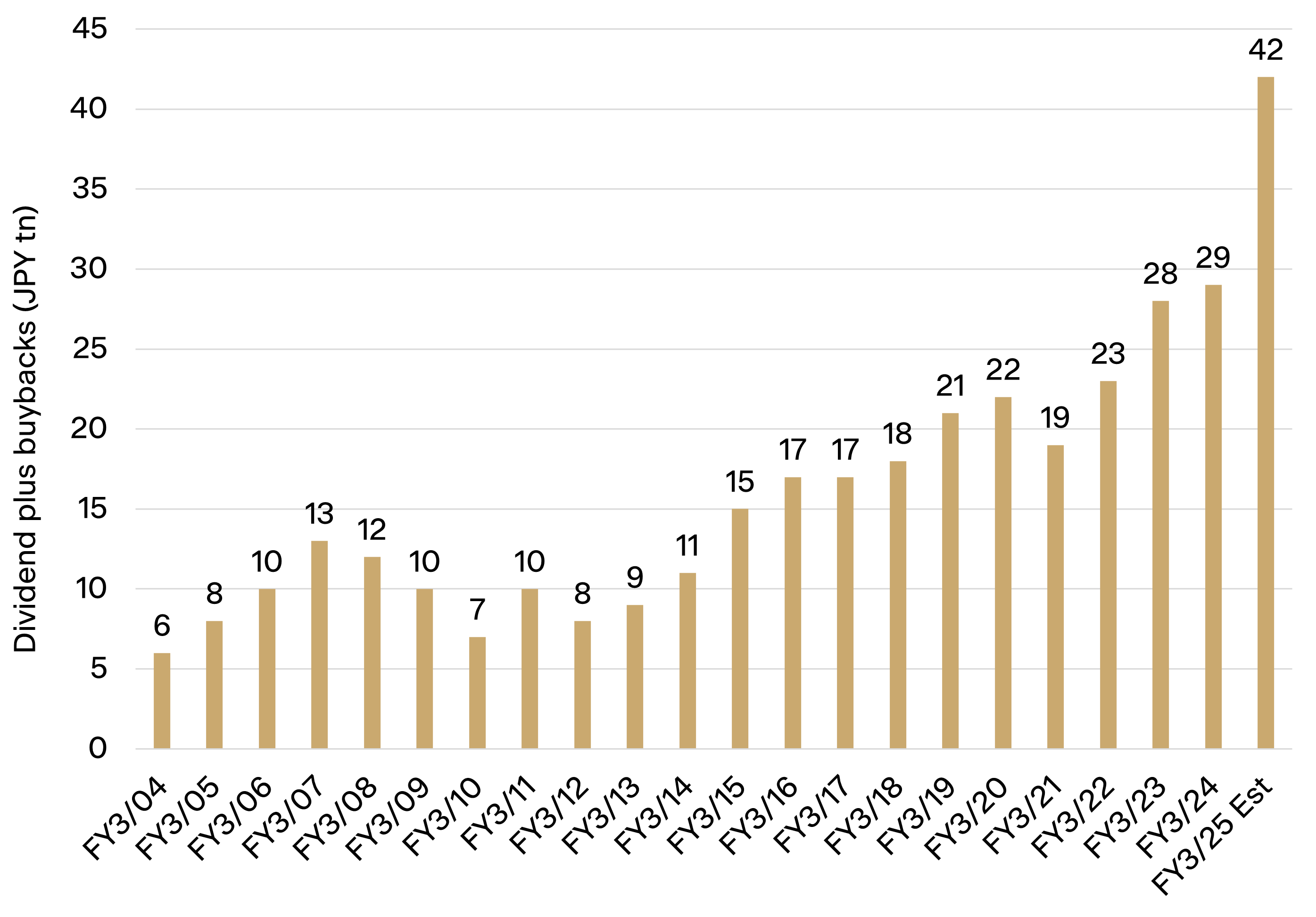

The Tokyo Stock Exchange’s (TSE) ongoing reforms are proving a powerful catalyst. In 2023, the TSE launched its “comply or explain” campaign, urging companies trading below book value to improve capital efficiency or publicly justify why they aren’t. The message was clear: lift return on equity, shrink bloated balance sheets, unwind cross-shareholdings and return capital to shareholders. Companies that ignore this pressure risk being publicly named, or increasingly, targeted by activists. We’re still in the early innings of what is likely to be a multi-year shift in capital allocation across corporate Japan. Buybacks have doubled over the past 12 months, and more companies are setting multi-year capital return plans. Yet more than half of Japanese companies still trade below book, suggesting the reform story has further to run.

Topix - Total aggregate dividends & buybacks by year

For active managers, it’s a rare alignment of top-down reform and bottom-up opportunity. Japanese software, in particular, has been fertile foraging ground. The country still lags global peers in cloud adoption, with many businesses relying on outdated infrastructure and legacy systems. As digitisation gathers pace and governance standards improve, the runway for high-margin, capital-light growth companies is expanding.

Separately, the government is pushing hard on cashless payments, aiming to lift penetration to 80% from around 40% today, well below the 60-70% levels already reached in most Western markets. E-commerce is similarly underdeveloped, accounting for just 9% of retail sales versus 15% in the US and more than 25% in the UK. These structural shifts are creating multi-year tailwinds for a small but growing group of domestic software champions, including one of the Fund’s holdings, GMO Payment Gateway (JP:3769), a leading Japanese payments processor serving both online and offline businesses.

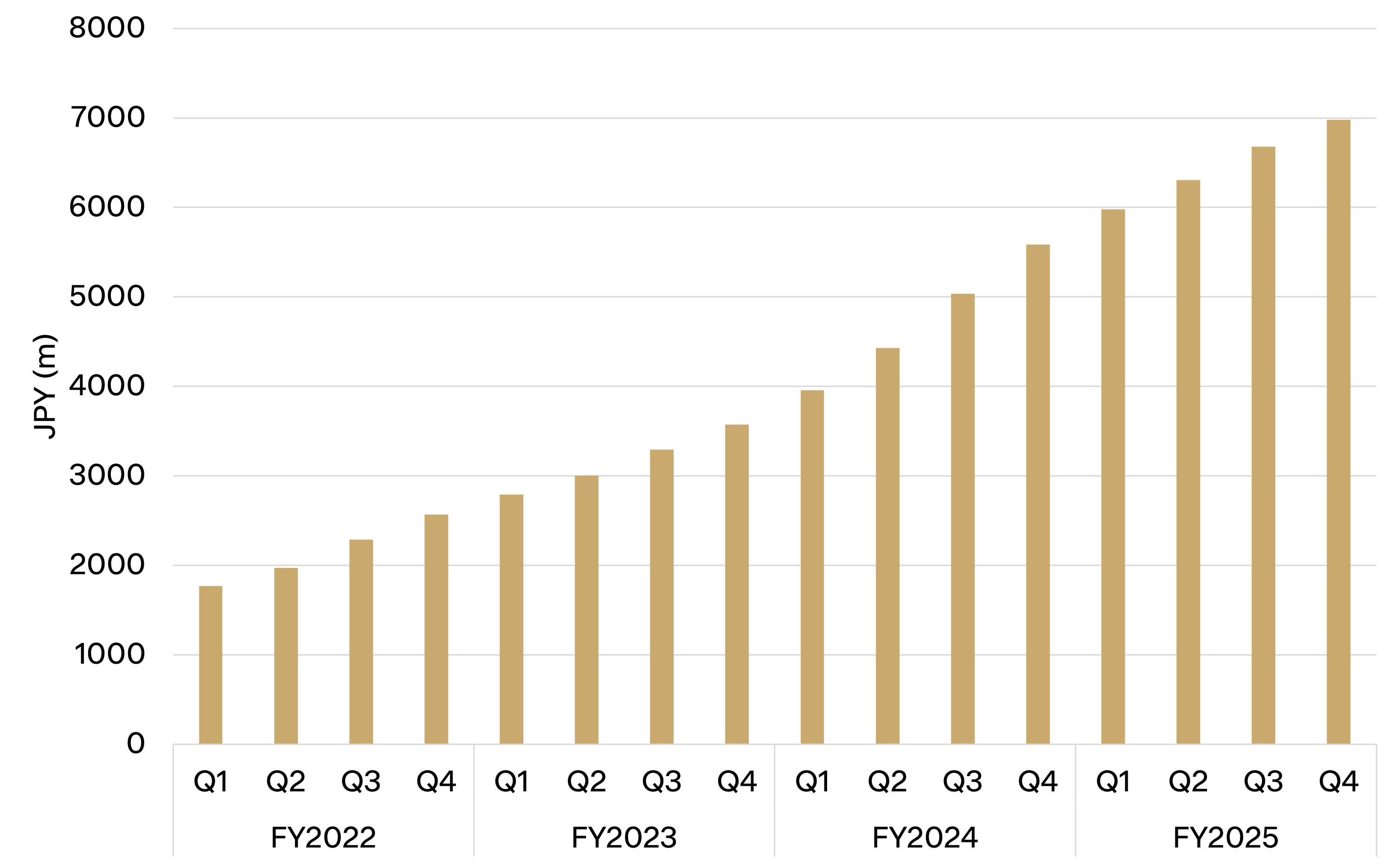

Two more of the Fund’s top contributors this year were Japanese software businesses benefiting from the country’s accelerating digital transformation. OBIC Business Consultants (JP:4733), a longerterm holding, is a conservative, highly profitable software company specialising in accounting and payroll solutions for small and midsized businesses. It added 1.0% to returns as it continued delivering steady, software-driven growth with strong margins. Shift (JP:3697), a newer addition, is Japan’s leading independent provider of software testing and quality assurance services. It’s a capital-light business scaling quickly in a fragmented market, and it contributed 1.1% to Fund performance before being sold.

OBIC Business Consultants cloud revenue by quarter

Japan’s labour market is also changing. A shrinking workforce, rising wages and a shift away from lifetime employment are pushing large corporations to modernise HR systems and embrace mid-career hiring. That’s creating a fertile environment for Visional (TSE:4194), an HR technology company offering platforms for recruitment and workforce management.

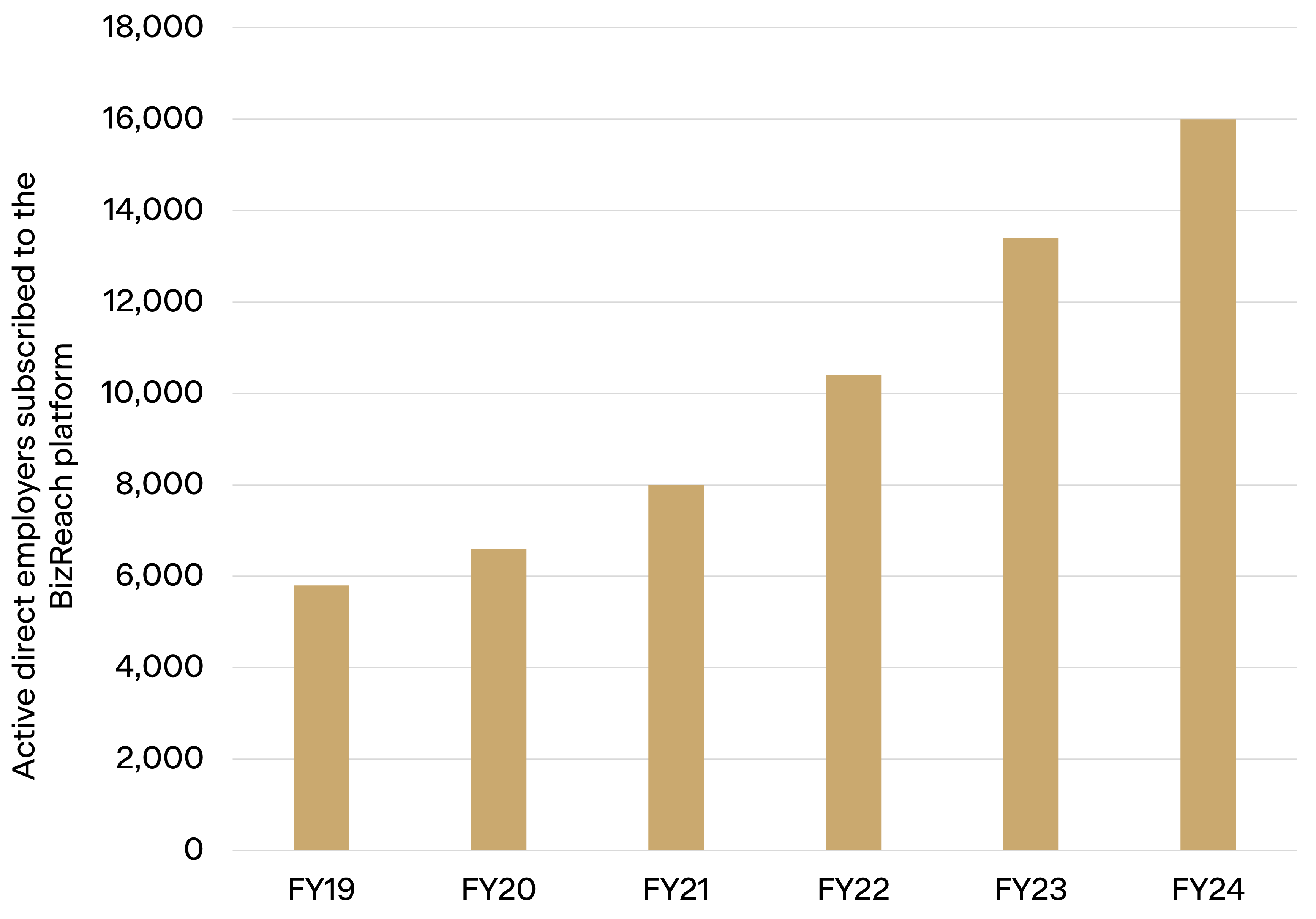

Despite its short tenure in the portfolio, Visional has already made a meaningful contribution. Its two core platforms, BizReach (Japan’s leading direct recruiting site for high-income professionals) and HRMOS (a cloud-based HR suite), serve over 16,000 paying clients and are building a sticky ecosystem across HR workflows.

Visional subscribers are growing steadily

It’s exactly the kind of capital-light, high-margin software business that we like. Growth has been consistent, margins strong, and management disciplined in reinvestment. For a business compounding earnings at around 20%, the valuation still looks undemanding. Visional has all the ingredients of a long-term compounder, and the broader structural tailwinds in Japan are only just beginning. Visional is now a top 10 holding in the Fund.

Between structural reform, improving governance, rising capital returns and an underappreciated runway for digital transformation, Japan is one of the Fund’s most attractive investment markets.

This is an excerpt from the June 2025 Annual Report