Passive flows and opportunity

Passive funds are the giants of modern markets, and they are here to stay. At Forager, we have taken the view that it is best to work with, not against, these funds. Therefore, long may they expand their footprint in equity markets.

Low-cost passive funds—and I’d include Australia’s superannuation giants in this category—are largely a force for good. Their relentless focus on costs has saved investors billions in fees. Given their enormous size, it’s entirely logical for them to stick to large, liquid companies. Take Australian Super as an example. As of 31 March this year, it had $367 billion in funds under management.

There’s simply no need—or point—for a fund of that size to venture into Australian small caps. Even if it invested $100 million in Forager’s

Australian Shares Fund, our 18% outperformance, would have earned its members just an extra 0.0049% for the year. Count the decimal points yourself.

Yet what’s logical for them creates opportunities for us. Think of it like the crumbs from a giant’s sandwich. For the giant, those crumbs are inconsequential. For a nimble ant, they can represent an enormous feast.

Over the past year, passive trends have helped us in three important ways.

Price-agnostic sellers

First, we’ve seen plenty of forced, price-insensitive selling at the smaller end of the market. This happens when stocks become too small for the giants’ portfolios, or when fund liquidations occur because super funds have given up on active small-cap managers.

Several high-profile small-cap fund closures occurred over the past 12 months as super funds pulled mandates. This created opportunities for us to add to existing investments at attractive prices—for example, in MotorCycle Holdings.

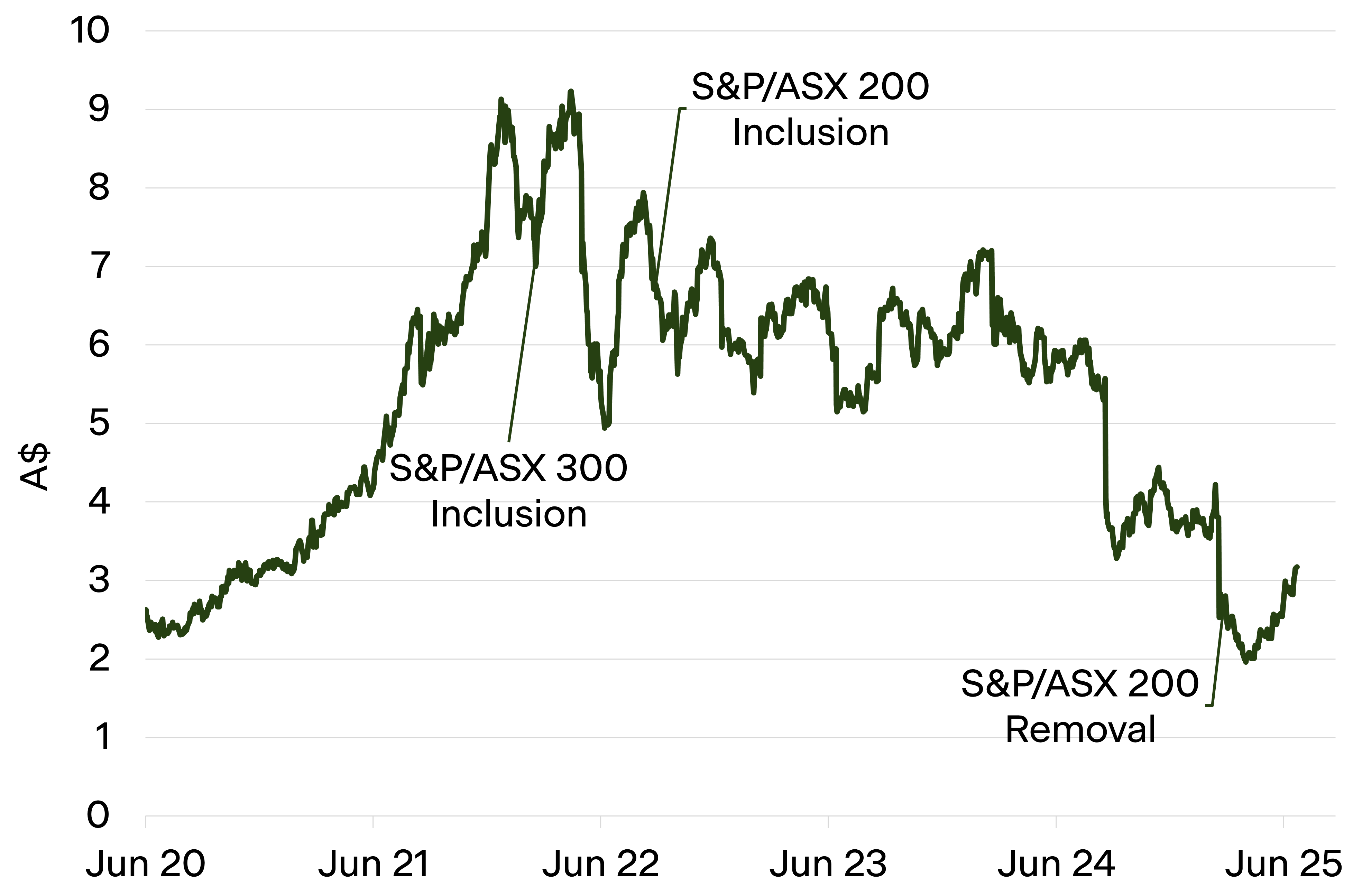

Companies at the bottom end of indices often experience sharp price declines as an initial, fundamentals-based drop is exacerbated by waves of passive selling. ASX-listed Johns Lyng, for instance, had a market capitalisation above $2 billion in mid-2022, enough for inclusion in the S&P/ASX 200 Index. By 31 March this year, it had been deleted from that index, with its share price down more than 75% from its peak(it bottomed, not coincidentally, on 9 April).

The business isn’t as good as investors thought when the share price was north of $9. But in our view, it’s not as bad as a $2 share price would suggest either. Most value investors would agree. Yet much of the price movement reflects passive investors who haven’t given valuation a moment’s thought.

Thematic waves

Another source of returns has come from the growing influence of thematic exchange-traded funds (ETFs). These funds allow investors to target sectors linked to themes like defence, cybersecurity, or artificial intelligence. While gaining popularity in Australia, they’re already significant players in US markets.

I’m far less convinced that thematic funds are a force for good. The whole point of index funds is to acknowledge that beating the market is difficult—and that keeping fees low matters most. Thematic funds charge significantly higher fees than broad index funds and appeal to investors who want to punt on the next hot sector. Almost by design, they attract a surge of money near the peaks and lose much of it at the lows.

That can create buying opportunities for us. Take Comfort Systems. I first met the management team of this NYSE-listed company at a broker conference in Chicago in November 2023. They provide a wide range of mechanical, electrical, and plumbing contracting services, specialising in HVAC systems.

My notes at the time read: Nice business, good management team, not sure about the special sauce, probably not cheap enough for us.

Forager’s International Fund Portfolio Manager, Harvey Migotti, met them again in November 2024. His assessment: Very good business, great management team, and strong long-term tailwinds from data centre construction and manufacturing returning to the US. The share price had doubled in the interim, but Harvey returned to Sydney convinced we needed to complete our research and be ready to act.

Then came Donald Trump’s renewed assault on global trade. Between 22 January and 4 April, Comfort Systems’ share price fell 46%. This company carries net cash on its balance sheet and has years of work locked into its order book. Yet when money flows out of the market, even good businesses get hammered. That’s when we get our chance to buy into companies with very bright futures. We’ve seen it across sectors—from building products to discretionary retail. When a theme falls out of favour, share prices across the sector tend to drop in lockstep, and the selling becomes indiscriminate.

Crumbs that grow large enough for giants

The third source of opportunity lies in identifying stocks that passive buyers will inevitably need to own a few years down the track. Consider the journey of Catapult Group.

In May 2022, the stock typically traded between $100,000 and $200,000 per day. Now, with Catapult firmly included in the S&P/ASX 300, it’s rare for daily volumes to fall below one million shares. With the share price up fivefold, that equates to more than $5 million worth of shares traded daily—and $10 million days are not uncommon.

Catapult’s business has progressed meaningfully, growing revenue nearly 20% per annum and delivering improved profitability. But index inclusion has been the mayonnaise on the sandwich. The increased liquidity firstly means larger small-cap managers can get interested. Then the passive funds need their share as well. Having traded at an undemanding two times revenue in 2022, Catapult now trades at a much more optimistic eight times the significantly higher revenue.

That “mayonnaise” will matter more as passive influence keeps growing. Forager will still invest in businesses that never make it into any index or super fund portfolio. Some of them, bought at the right price, will deliver excellent returns. There’s already plenty of money trying to arbitrage which stocks will be added or dropped whenever index providers rebalance. That’s not our game.

But when we’re looking three to five years ahead, we always ask: Could this business ever attract passive buying? Index inclusion can significantly amplify profits from successful investments. And at our relatively small size, it can add a meaningful boost to total portfolio returns.

The shift toward index funds and giant super funds isn’t likely to reverse. In aggregate, money will likely keep flowing out of the small- cap end of the market. For those of us with loyal, long-term clients, that makes for particularly fruitful foraging.

This is an excerpt from the June 2025 Annual Report and also appeared on Livewire Markets