A large part of the software sector deserved its correction.

At the peak in late 2025, many software businesses were extremely optimistically valued. Businesses were ranked using revenue growth alone, often with limited regard for profitability. Where profitability was contemplated, it usually ignored one of the largest expense items for these companies - the prodigious amount of shares issued to staff as compensation each year. The prevailing view was that software economics were structurally superior and largely insulated from disruption. That proved too optimistic.

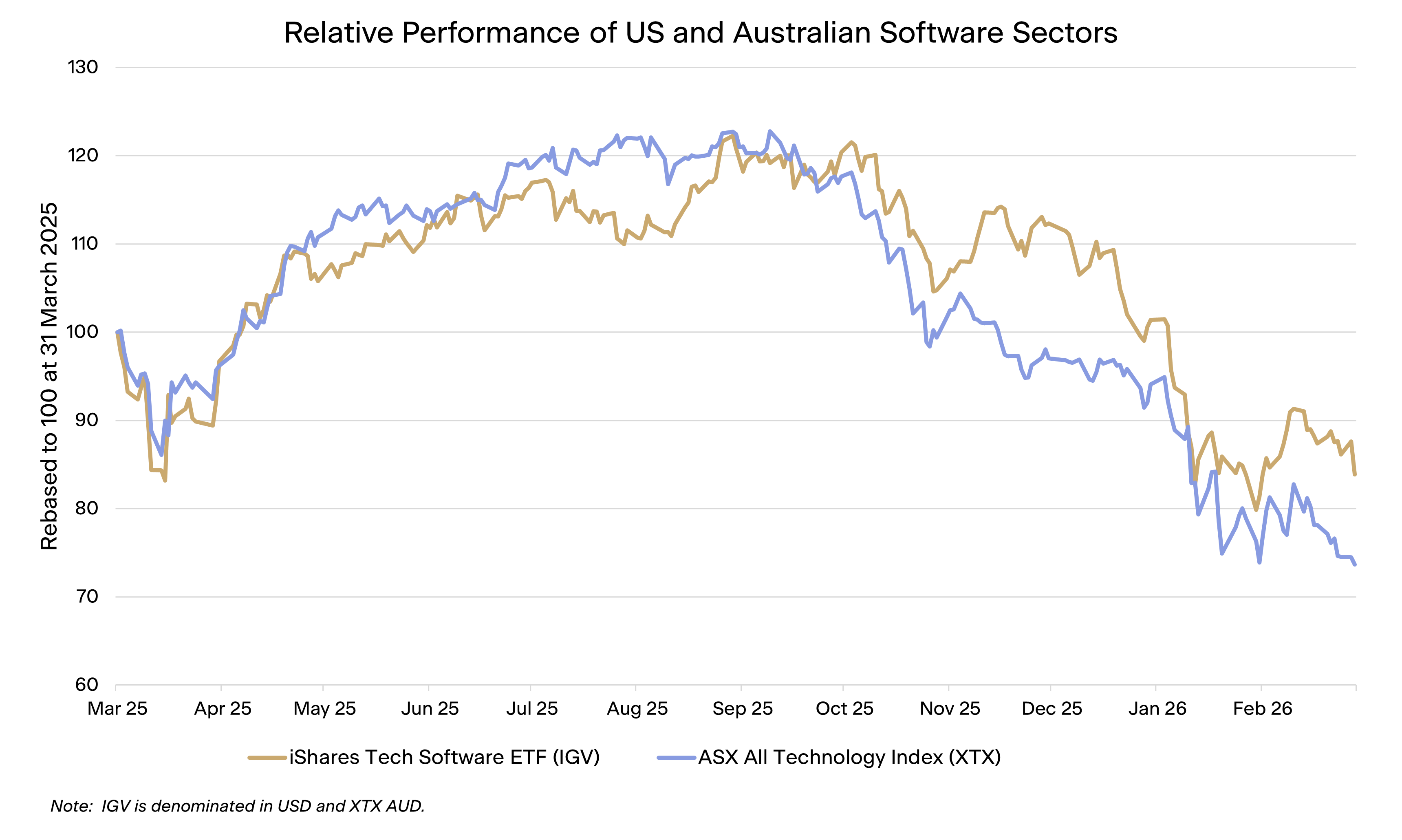

Now the narrative has shifted sharply in the opposite direction. So much so that the market reaction over the past six months is being dubbed the Saaspocolypse.

Source: Bloomberg

The financial press is increasingly populated with examples of companies reducing software spend by building internal tools. Developers are demonstrating how quickly functional alternatives to established products can be assembled using AI coding agents. There is a growing view that artificial intelligence will, at best, compress margins for many incumbent products and, at worst, disrupt them the way the internet disrupted the newspaper industry.

It will come as no surprise that Forager is sharpening the pencils and has already added a couple of investments to both portfolios. Pessimism is where we thrive.

Working out whether the pessimism is undue or warranted is the hard part. But without it you don’t get great investment bargains.

The key is not to argue that the risks are misplaced. Many are real and will play out. The opportunity lies in identifying the subset of businesses where those risks are either overstated or already reflected in price.

At Forager, we are focused on four characteristics when assessing software opportunities in this environment.

1. High value, low cost

The first is software that is deeply embedded in customer workflows, yet represents a small proportion of total spend.

Accounting platforms such as Xero (ASX:XRO), MYOB and Sage (LSE:SGE) are clear examples. These products typically cost small businesses tens of dollars per month and sit at the centre of financial operations - handling invoicing, payroll, compliance and reporting.

The economic trade-off for customers is straightforward. The absolute cost is low, while the operational importance is high. Replacing these systems introduces risk and disruption for limited financial benefit.

This dynamic is reflected in the underlying economics. Xero has historically delivered strong revenue growth with gross margins above 80% and low churn. Sage, which we have recently added to the Forager International Shares Fund, serves more than 6 million customers globally and generates consistent free cash flow with operating margins above 20%.

Where software is inexpensive, mission-critical and priced for business size rather than number of users, pricing pressure tends to be limited, even as development costs fall.

2. Structural switching costs

The second characteristic is high switching costs.

Software rarely operates in isolation. Over time, it becomes integrated across multiple systems, accumulates data and shapes internal processes. The cost of replacement is therefore not simply the price of a competing product, but the time, expense and operational risk associated with transition.

Bravura Solutions (ASX:BVS) illustrates this dynamic. Its software underpins core functions for wealth managers and super funds - industries with complex regulatory requirements and low tolerance for operational failure. System replacement can take years and involve significant cost.

In this context, the ease of building new software is less relevant than the difficulty of displacing existing systems. Customer inertia, supported by genuine switching costs, remains a meaningful source of durability.

3. Moats beyond software

A third area of focus is businesses where the competitive advantage does not reside in the software itself.

CAR Group (ASX:CAR) provides a clear example. The company’s current market capitalisation is north of $8bn, even after a significant share price retraction. Even if the project were run by the Australian Bureau of Meteorology, even in the days before AI coding, you could replicate carsales.com.au for a few tens of millions. The value is clearly not in the cost of the code. Carsales value instead lies in its position within the automotive ecosystem - connecting a large audience of buyers with a broad base of dealers and private sellers.

This network effect has been built over decades and is reinforced by scale. High levels of traffic attract listings, and listings attract further traffic.

Auto Trader (LSE:AUTO) in the UK demonstrates the same characteristics, generating pre-tax profit margins above 60% in a business where the technical barrier to entry is relatively modest.

These advantages are not immutable. They depend on sustained user engagement and relevance. The eyeballs can potentially transition to AI models, or AI agents can handle more of the looking. But they are not easily or quickly eroded by incremental improvements in software development capability.

4. Value, the sooner the better

It’s our conclusion that the stockmarket Saaspocolypse is unlikely to be an industry wide operational Saaspocolypse. Some businesses will undoubtedly suffer. Some will be beneficiaries of the AI tools now available. That doesn’t make it as simple as buying the survivors.

Even after a significant de-rating, parts of the sector remain far from cheap. And the excessive stock based compensation practices don’t seem to be abating (we have seen some companies increase the amount of shares they are issuing to compensate staff for a lower share price).

We are looking for stocks that are cheap. And the more of the value we get back in the near term, the better.

Bond investors use a concept called duration to assess interest rate sensitivity of bonds. It represents a weighted average life of a bond’s cash flows (so a 30-year bond has a much higher duration than a 2-year bond). If interest rates go up, those longer dated cash flows are worth less in today’s dollars.

The same concept applies to the stock market, which is why you see “growth” assets generally underperform in a rising interest rate environment - their value is dependent on cash flows generated in the distant future. It also applies to their operational risk.

Businesses priced on long-duration assumptions require a high degree of confidence in their ability to sustain growth and competitive positioning over extended periods.

That confidence is harder to justify in a rapidly evolving technological environment.

By contrast, companies that generate meaningful cash flow today and are capable of returning a substantial proportion of their market value within the next decade offer a more balanced risk profile.

Sage and Auto Trader are examples where, based on current earnings and growth expectations, a significant portion of today’s valuation could be returned to shareholders through free cash flow over a 10-year period. This reduces reliance on long-term forecasts and limits exposure to distant disruption scenarios.

The Forager investment thesis

Forager’s International Shares Fund already had a significant investment in Japanese software companies. They continue to grow rapidly, are highly profitable and don’t have the excessive stock based compensation practices of their US cousins. That hasn’t stopped their share prices getting whacked over the past few months, making topping up what we already own the first way we are taking advantage of the opportunity.

Outside Japan, we have added a few undervalued UK and Australian stocks to both portfolios and have the analysis framework in place for more. The shift in the software narrative from "structural superiority" to "imminent disruption" has already created some attractive investment opportunities. Lower prices and an increased focus on shareholder returns would provide the confidence to add more.

If you are interested in finding out more about opportunities the Forager investment team are finding in the Saaspocalypse, subscribe to our investing community