The ASX Small Ordinaries Accumulation Index is having a decent year. At least that's what the headline suggests.

The index is up around 10% this financial year, comfortably ahead of a 5% return for the large-cap skewed All Ordinaries Accumulation Index. Dig a little deeper, though, and the picture looks very different. Small resources stocks have rallied more than 50% and now account for around 35% of the index, well above their historical weighting of closer to 20%. Small industrials, meanwhile, are down around 5%. Technology stocks have fallen almost 30%.

Greed and panic have both been hidden by the average.

Investors have no shortage of concerns. Consumer confidence remains fragile, interest rates have risen sharply and the conflict in the Middle East continues to create uncertainty. The budget adds yet another layer of anxiety into the mix.

Forced sellers, especially of small cap industrials, have been seen around the market recently as some funds face investor redemptions or closure. Tax-loss selling continues to weigh on some stocks as well.

In environments like this, investors often sell first and ask questions later. Smaller companies tend to bear the brunt of that caution. On average, the index sits below its long-term valuation multiples and is unusually cheap relative to larger companies.

In December the Forager Australian Shares Fund held approximately 19% of the portfolio in cash (including a company in the later stages of a takeover).

Today cash sits at about 5%.

Revisiting Technology

Technology has become one of the market's most controversial sectors.

Much of the debate centres on what has become known as the "Saaspocalypse" - the idea that artificial intelligence will permanently damage software businesses by making software development cheaper and reducing barriers to entry.

There is some truth to that concern. Some software companies will struggle. Others, however, may emerge stronger.

The best software businesses solve important problems at a relatively low cost for customers. Catapult (ASX:CAT) is a good example. The company provides wearables and video analysis tools to professional sporting organisations around the world.

For elite clubs spending tens or hundreds of millions of dollars on players, Catapult's average annual spend of around US$30,000 per team is a rounding error. The hardware and software suite helps improve performance, reduce injuries or gain a competitive advantage, so remains very compelling.

After selling out of Catapult as valuations reached stretched levels late last year, the business is now the second-largest investment in the Forager Australian Shares Fund.

Switching costs matter too. Bravura Solutions (ASX:BVS) provides mission-critical software to wealth managers and superannuation funds. These are systems that sit at the heart of client administration and reporting. Replacing them is expensive, disruptive and risky. Trust becomes an important competitive advantage, particularly in heavily regulated industries.

Having also exited Bravura late last year the company is now a top-five investment for the Fund.

Some technology businesses possess moats that extend well beyond software. Hipages Group (ASX:HPG) operates Australia's largest online marketplace connecting tradies with customers. The value lies less in the underlying technology and more in the network itself. Homeowners post jobs because tradies are there. Tradies participate because that's where the jobs are. We have taken the opportunity to increase the Fund’s investment in the business this year.

Since the start of the calendar year the Fund’s software investments have moved from 3% to 16% of the portfolio.

More Capital for Existing Investments

Capital has been deployed across a handful of existing investments outside of software too.

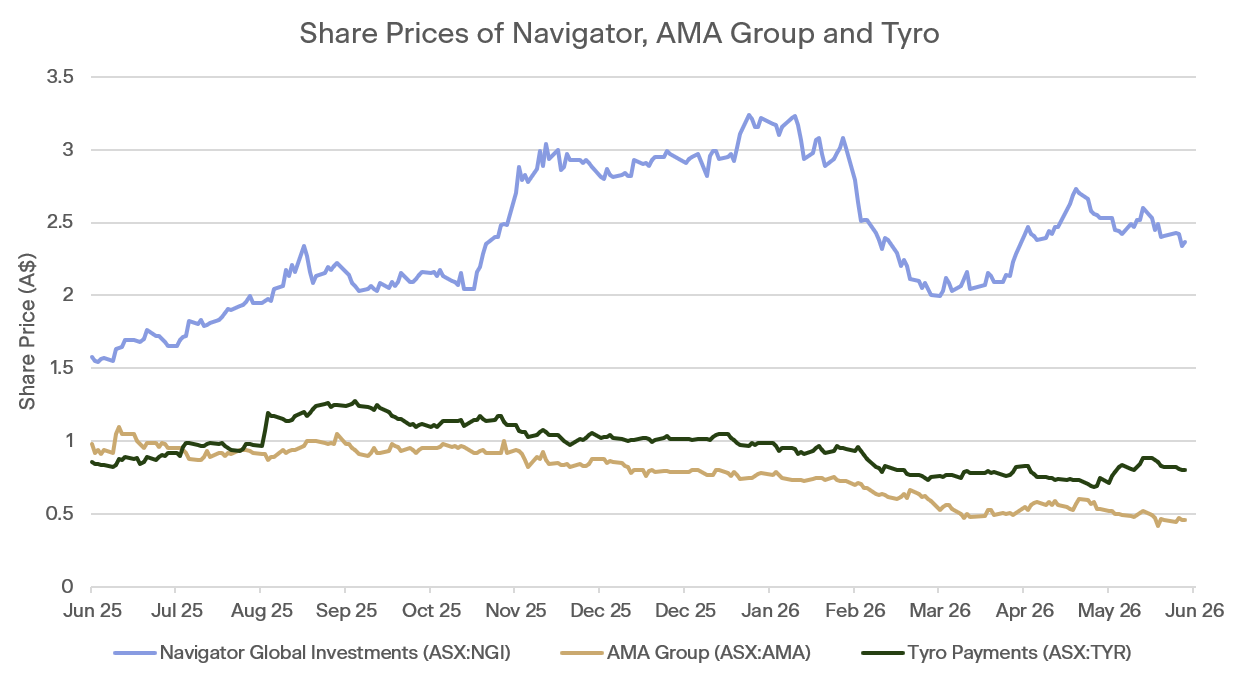

Despite an accretive acquisition, alternative fund manager investor Navigator (ASX:NGI) is down by more than a quarter from prior peaks. The business continues to benefit from growth in assets under management and all-important performance fees, while the acquisition should enhance scale and importantly diversify earnings.

Panel beater AMA (ASX:AMA) showed decent progress in its first three quarters and has maintained guidance despite the threats from higher oil prices. Operational improvements should continue to flow through the business, improving margins over time. The stock is sitting more than 60% below recent peaks.

Payment terminal provider Tyro (ASX:TYR) has been through a few years of regulatory uncertainty. The RBA’s recently released payments review puts Tyro in a good position to gain market share. A new CEO is in place to build on the operational momentum, especially in health and new verticals. The stock is down about 35% from recent peaks.

Source: Bloomberg

The attractiveness of the opportunities available to the Fund is similar to what we saw in late 2022 and early 2023, when sentiment towards small companies was particularly weak. That period of pessimism set the foundations for many years of strong performance.

Takeovers Shine a Light on Hidden Value

Small cap public company investors are not the only potential owners of unloved and underappreciated stocks. The past few weeks have seen takeovers of smaller industrial companies ramp up.

Recreational vehicle operator Tourism Holdings (ASX:THL) saw a bid from a private equity firm, which has paired up with a major shareholder. The first bid came twelve months ago at NZ$2.30 per share. The bid price now is NZ$3.10 per share, and much closer to the board’s view (at the time) of value being “well north of $3.00 per share”.

Readytech (ASX:RDY), enterprise software provider across a few industries, has disappointed investors with slower revenue growth and rising costs over the last few years. The resulting depressed valuation attracted the likes of Topicus (TSX:TOI), a spin-out of Canadian vertical software behemoth Constellation Software (TSX:CSU). The bid, at $2.00 per share for the whole business or $1.75 per share for a minimum of 50.1%, has been rejected by the board. But it does illuminate the strengths of the business, unfortunately hidden under a bloated cost base.

And foreign exchange provider OFX (ASX:OFX), deep into a technology transition while losing market share to competitors, is running a well-progressed strategic review with multiple interested parties. The business retains a valuable client base, licenses around the world, and a new platform. The process is due to complete this month.

As in the past, if public company investors fail to recognise the value on offer, that value can be realised by bidders. More takeovers are likely if the malaise continues.

Markets are rarely comfortable when the best opportunities emerge. Small industrials remain out of favour, technology stocks are being priced as though disruption is inevitable and investors continue to focus on near-term risks. Of course, investing during periods of volatility or when certain sectors are out of favour always carries risks, but from a Forager’s perspective, we believe this environment has opened up some great opportunities in unloved and underappreciated stocks.

Investors wishing to update their Distribution Preferences for the Forager Australian Shares Fund can do so by logging into Automic, selecting "Reinvestment Plans" and following the prompts