After three very strong years of both absolute and relative returns, you might argue a difficult one was due. If that is your way of thinking, the 2026 financial year certainly delivered for Forager. Both funds returns were negative for the year, while the market delivered decent returns in Australia and very strong returns internationally.

Part of that was self inflicted. One mistake cost significantly more than the largest winners in both funds. In recent years that ratio was in our favour. There were mistakes, but they were less costly and the winners were much larger.

Far more important was a lack of exposure to the hot sectors of 2026. If you weren’t invested in artificial intelligence (AI) stocks and/or commodities, it was almost impossible to make money.

Forager does, as you know, have wide investment mandates and some of the second-order winners from the AI revolution were contracting businesses squarely in our circle of competence. The transformational importance of generative AI, the technology behind Chat GPT and Claude, has been clear to us for a long time. It is being widely used in, and has had a transformative impact on our business. We owned a couple of stocks in the Forager International Shares Fund that were big winners, but largely missed the first, more rational part of this boom.

What was a boom has become a bubble, though, with investor euphoria and FOMO (fear of missing out) reaching extreme levels in recent months. The SpaceX IPO is the poster child. A few days after its much-hyped float, the company—which currently generates US$20bn of revenue and slid back into deep losses last year—was “valued” at more than US$2 trillion (while 90% of the total addressable market outlined in its IPO document was AI, SpaceX’s xAI is currently a long way behind the current industry leaders).

We make no apology for not participating in the FOMO. In fact, we want to be as far away from it as possible.

How the bubble bursts

There is no questioning the transformative nature of this technology. Like electricity, the automobile and the mobile phone, it will become ubiquitous and change our lives in ways that we don’t currently anticipate.

As famous investor Jeremey Grantham pointed out on a recent Odd Lots podcast, while some see the transformative nature of the technology as a justification for investor optimism, all great stock market bubbles have a genuinely transformative technology to spark them. You don’t get a genuine bubble without a technology that will change the world, preferably one that billions of people can understand.

This one is going to run head first into some economic realities over the next few years. Trillions are being poured into data centres, chips, and AI infrastructure.

First, that spend is already crashing into the constraints of the physical world, where supply chains and public opinion get in the way of the tech industry’s traditional “move fast and break things” mantra. Those constraints may disappoint investors extrapolating the current breakneck growth over the coming years.

Second, much of the excitement comes from the fact that AI can do such a wide range of activities, from writing your job application to building a website to answering all of your customer queries. Yet it is energy hungry and, for many tasks, inefficient. Most of us are not paying the full economic cost of the technology while the providers endure losses in their race to grab market share. Even with a subsidised cost, we often run out of “tokens”, or usage capacity, at Forager within the first few hours of the day. We have started to ration the use to the tasks from which we get the most benefit, and many businesses are slowly working out that a cheap resource in India will make more economic sense for quite a while yet.

The technology is still in the rapid adoption phase and will be for several years, but any suggestion that demand growth might slow would be a huge blow to the share prices of those benefiting most from the industry’s capex boom. Most of them were mediocre businesses before the AI boom came along.

Will a great technology be a great business?

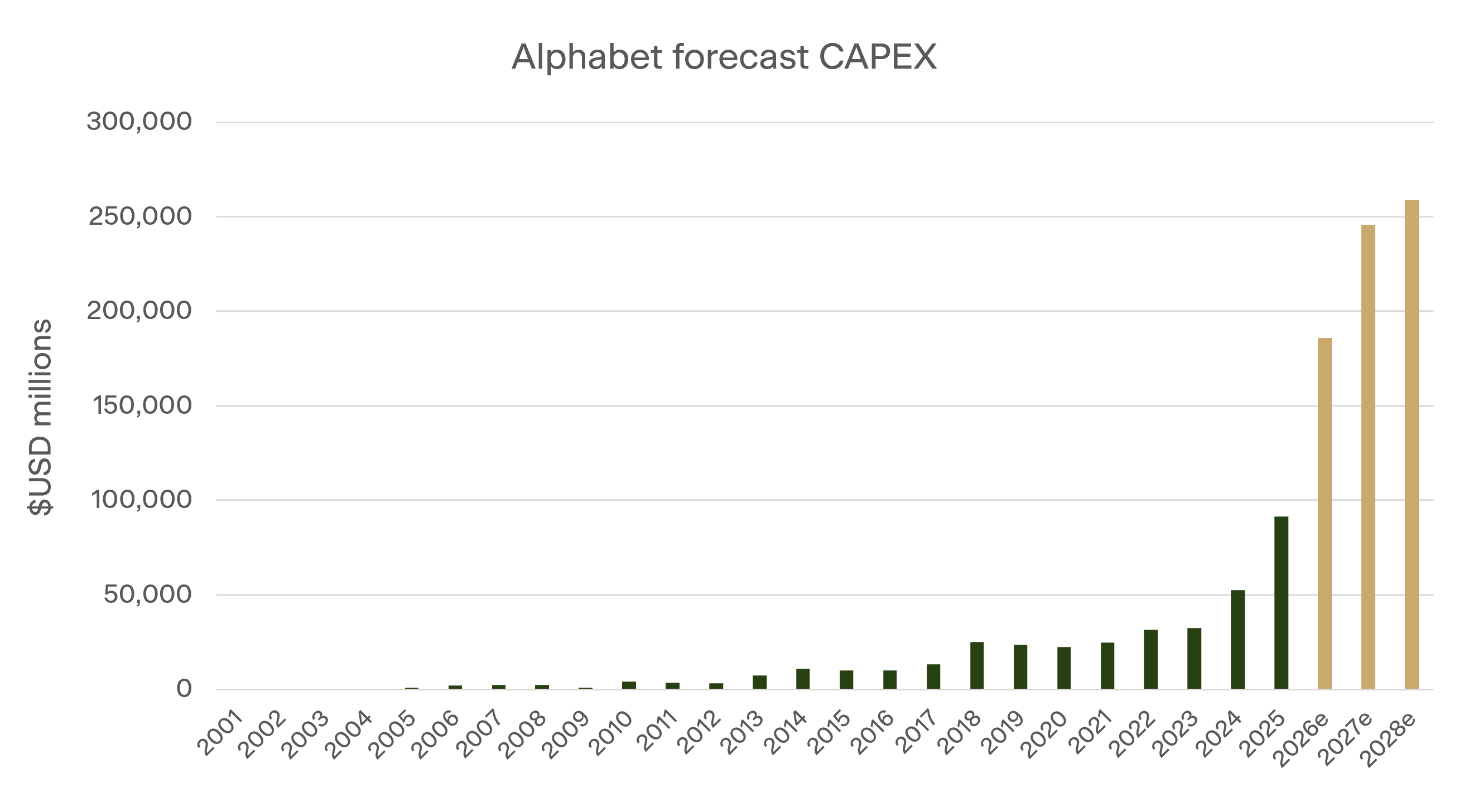

Finally, for the AI giants, this may be a much more difficult business than they are used to. Alphabet, the owner of Google, is one of the best businesses the world has ever seen. It is effectively a monopoly on the global online advertising industry. Building that monopoly cost very little in the way of tangible capital, the barriers to entry are almost insurmountable and it has generated hundreds of billions of free cashflow in its 25-year history.

It, alongside OpenAI (ChatGPT) and Anthropic (Claude) is one of the three global leaders in the AI revolution. So far, it is turning out to be a very different business.

Source: Bloomberg

Alphabet has told the market it expects to spend US$185bn on capital expenditure in 2026 and significantly more than that in 2027. In the next two years it will spend more on capex than it spent in the previous 24 years combined. It is becoming a highly capital intensive business and the competitors’ business models look exactly the same.

Will that spend generate outstanding returns? That depends on whether the AI industry ends up being a monopoly like the online advertising industry or a competitive capital sink like the automobile industry. For the sake of us consumers, the latter would be a far better outcome and, so far, it is looking nicely competitive. That could change, of course: Google had plenty of competitors in the early days. But any suggestion that the return on the trillions of dollars being thrown at the AI industry will be anything less than stellar could rapidly pop the bubble.

Calling a top is a fool's errand, and we have no intention of trying. But there is a more useful question for valuations-based investors than when the exuberance ends. It is: what kind of bubble are we in?

To understand the playbook from here, it helps to look at the two great market meltdowns of the last quarter-century. They were completely different beasts.

2000: the stockpicker's paradise

The dot-com crash was a spectacular time to be a value investor—not in the rear-view mirror, but looking forward. If you were sitting in boring, old-economy value stocks, you preserved capital right through a brutal tech meltdown that saw the Nasdaq fall roughly 78% from its peak and the broader S&P 500 drop close to 49%.

Value stocks went in with ridiculously low starting valuations while everyone else was chasing eyeballs and dot-com promises. That set up the 2003–2006 period, where value trounced every other style.

The pre-GFC bubble was the opposite—it set the whole market up for a horrible decade and value stocks were set to perform the worst. Back then, Grantham called it the "Everything Bubble," and he was right. The mania wasn't isolated to one hot sector, so nothing was cheap and there was nowhere to hide. Everything suffered through the 2007–2009 Global Financial Crisis.

Where we stand today

So which one is this?

Thankfully, today feels a lot more like 2000 than 2007. We aren't quite at the bargain-basement levels of 2000, but the crucial point holds: the current hysteria hasn't caught up with everything. It has, in fact, sucked the oxygen from most other parts of the market and there are plenty of places to hide from the exuberance.

While the crowd fights over the same handful of AI darlings, we are finding an abundance of sensible, cash-generative businesses that should do well relatively—and perhaps even absolutely—in any meltdown. Look around the world and you'll see islands of value the momentum crowd has simply ignored.

Take the global "SaaSpocalypse." An indiscriminate sell-off has hammered the sector, from Japanese small-cap software providers like eWeLL, Visional, and Obic Business Consultants—highly profitable businesses delivering strong double-digit earnings growth, whose multiples have been compressed simply because the businesses have the word "software" in the description—to hardware-heavy tech businesses like Australia’s Catapult. It's a similar story in old-school value sectors outside tech, where European bank stocks, US building materials and the UK market as a whole trade at pessimistic multiples despite solid fundamentals.

As the bubble has grown, we have sold what little exposure we had. As long as it goes on, you should expect both funds to continue their underperformance. We've never minded looking out of step with the crowd if it means staying disciplined and avoiding overvalued giants. We are entirely comfortable being unfashionable in the short term to make sure we're buying the right businesses at the right prices. When the bubble bursts, you should expect us to deliver a reversal.